.svg)

.gif)

Introduction

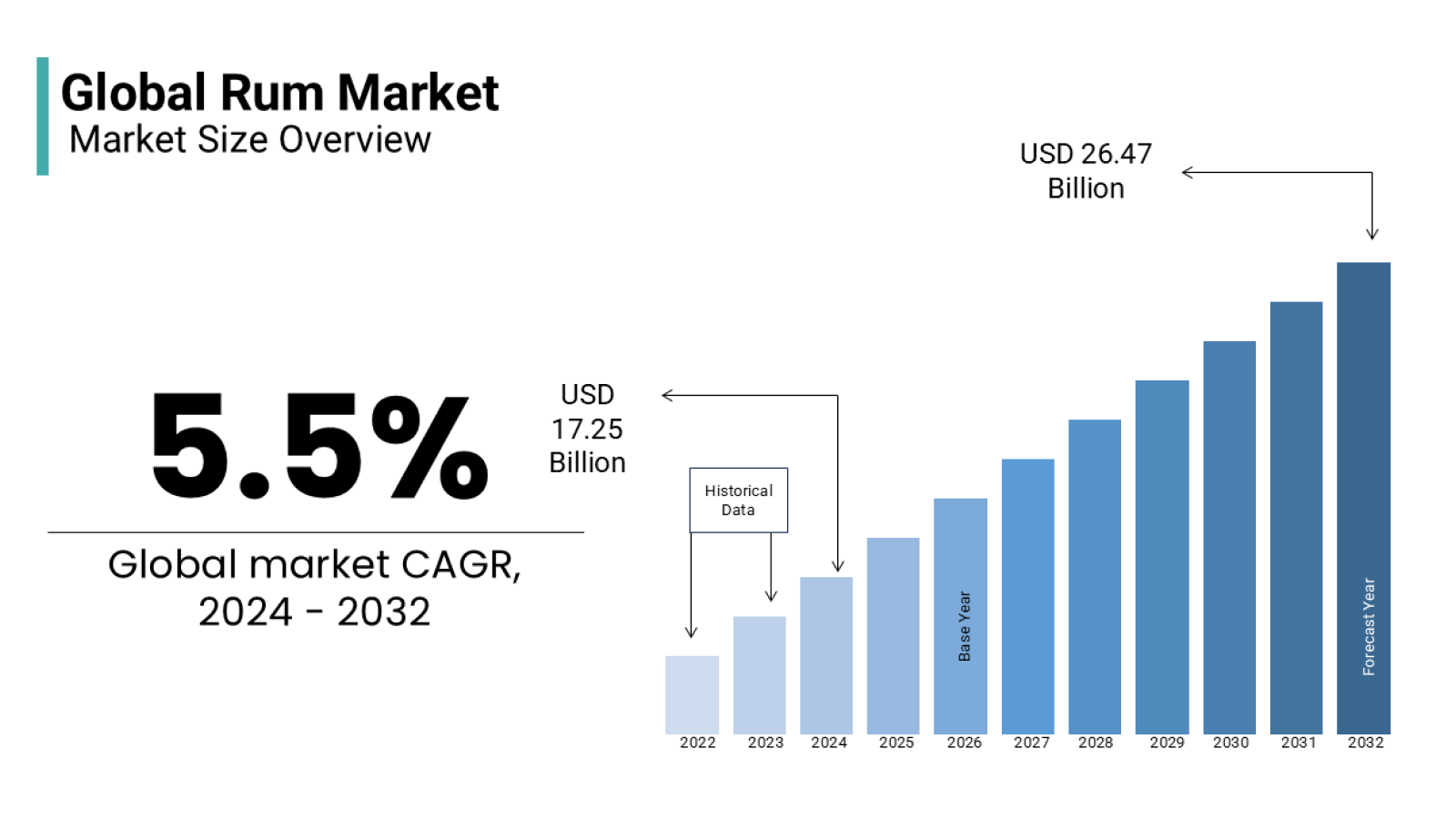

The global rum industry is charting an exciting new course as it heads into 2026. After a period of steady growth, the market showed some signs of cooling in 2024-2025, yet analysts remain optimistic about the road ahead. In fact, forecasts suggest the global rum market could expand from roughly $17.3 billion in 2024 to nearly $28 billion by 2033, a healthy CAGR of about 5.5%. This outlook reflects not just growth in volume, but a transformation in the quality and diversity of rums being produced and consumed. Rum, long associated with carefree cocktails and tiki bars, is evolving into a more sophisticated spirit category with premium offerings and innovative expressions leading the charge.

Several powerful trends are shaping the rum landscape as we move into 2026. From the ongoing premiumization drive and inventive new flavored rums, to the boom in ready-to-drink cocktails and even low/no-alcohol alternatives, producers are innovating to meet changing consumer tastes. At the same time, issues like sustainability, authenticity, and the complex regulatory landscape are coming to the forefront, forcing brands to adapt in how they source, label, and market their rums. In this report, we will review 2025’s rum market performance, delve into regional highlights (with a focus on the US, UK/Europe, and Asia-Pacific), and explore the key consumer and innovation trends. We’ll also examine marketing strategies (from rum festivals to digital campaigns), and candidly assess the challenges - from heavy competition to economic pressures - that rum players must navigate. The goal is to paint a comprehensive picture of what 2026 holds for rum and beyond, grounded in expert insights and the latest data.

The Global Rum Landscape: 2025 in Review & 2026 Projections

In 2025, the global rum market remained on a growth trajectory, albeit with some regional variability. Market analysts estimate the category reached around $14.6-15.3 billion in 2025, and is on track to grow roughly 4-6% annually in the near term. By 2026, global rum sales are expected to rise to the mid-$15 billion range, continuing a steady post-pandemic recovery. This growth is underpinned by consumers’ renewed interest in spirits with character and heritage - attributes rum has in abundance. As one industry expert put it, “Premiumisation remains the defining trend for the category”, with drinkers gravitating toward higher-quality rums and unique expressions. Indeed, premium and craft rums are identified as major growth drivers in the forecast period.

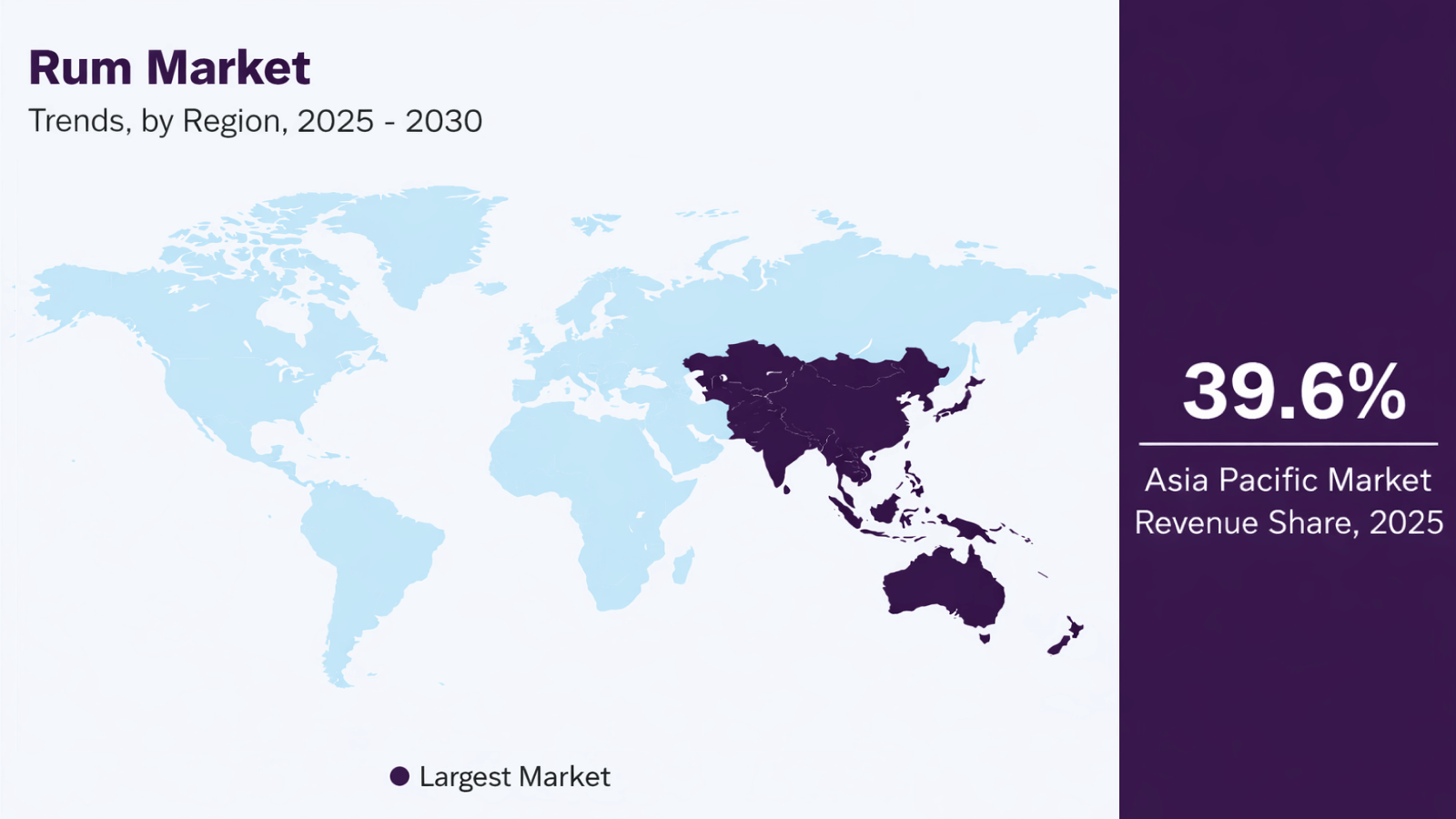

However, 2025 also highlighted an uneven performance across different markets. In general, Europe and parts of the UK saw dynamic growth, while the US market stagnated or even declined slightly. Asia-Pacific has solidified its status as the largest rum-consuming region, accounting for about 39.6% of global rum sales. By contrast, North America and Europe together make up roughly another one-half of the market (with Europe recently overtaking North America). Notably, Asia-Pacific was the largest regional market in 2025, and Europe was the fastest-growing region for rum, reflecting a surge of premiumization and cocktail culture in European countries. These regional dynamics signal that rum’s fortunes are rising in some areas even as others lag behind - a theme we’ll explore in detail in the next section.

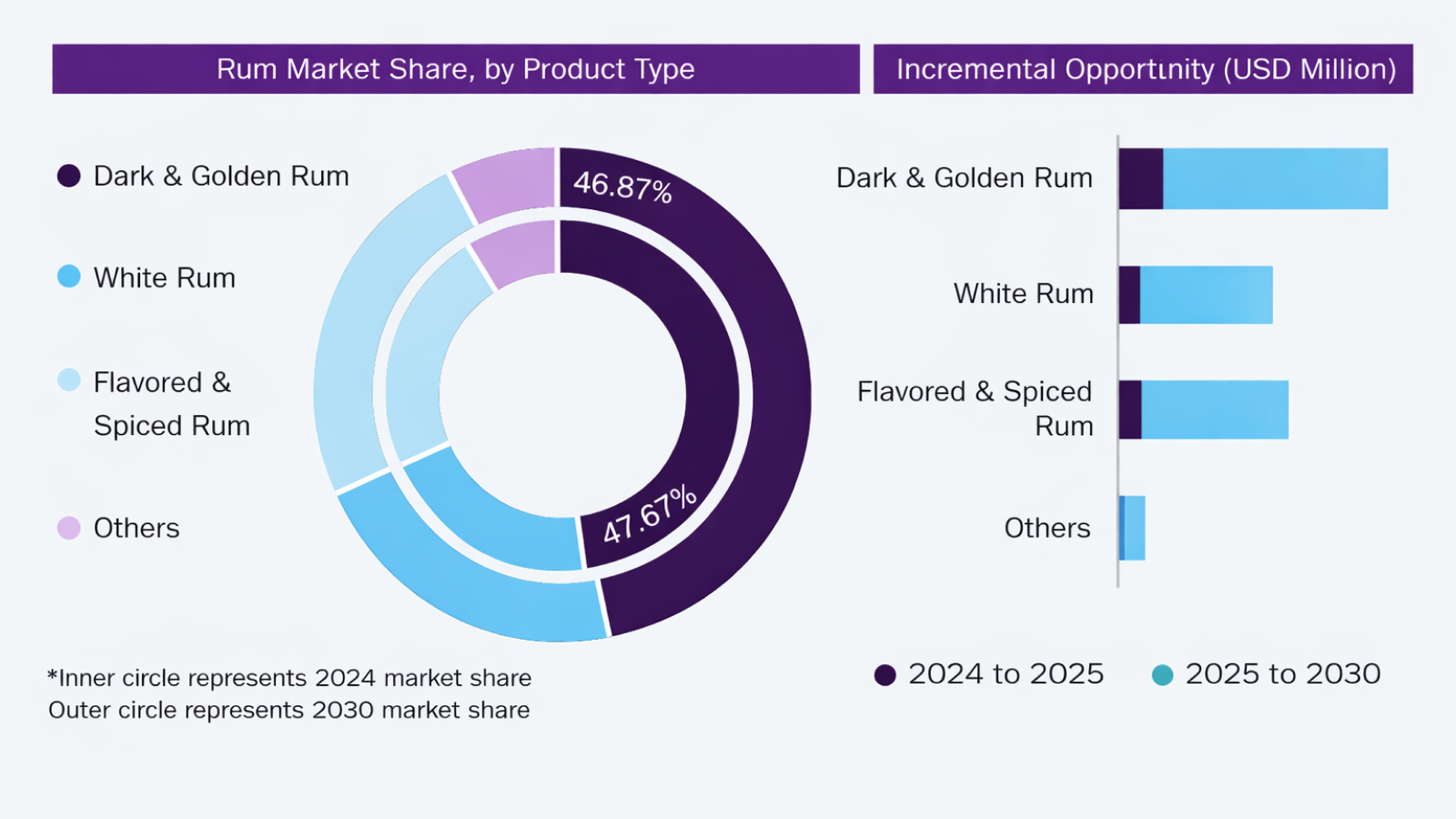

In terms of product mix, dark and golden rums command the largest share of global revenue (nearly 48% in 2024), and this segment’s strength continued into 2025. Consumers worldwide are showing appreciation for dark, aged rums, which often boast richer flavors and provenance stories. White rums still sell in high volumes, but value growth is slower as this segment is more associated with value-priced “mixers.” Meanwhile, spiced and flavored rums - once seen as entry-level or novelty products - have gained serious traction and are growing on par with the overall market (~4.7% CAGR expected through 2030). The introduction of new exotic flavors (tropical fruits, spices, dessert-inspired notes) has helped broaden rum’s appeal to younger and more experimental drinkers. Off-trade (retail) channels remain dominant for rum distribution (about 79% of sales in 2024 were in off-premise outlets), but on-trade (bars/restaurants) made a notable post-COVID comeback in 2025, especially as cocktail culture resurged.

Crucially, 2025 underscored that rum’s image is gradually changing. Producers large and small are moving away from gimmicky pirate tropes and “nautical” branding of the past, and instead highlighting quality cues - traditional production techniques, single-origin ingredients, and the spirit’s rich history. This repositioning has started to pay off in attracting younger consumers: those aged 25-34 now account for the largest share (around 20.7%) of rum drinkers, as they respond to these premium, authentic offerings. For example, new brands like Ten To One Rum, and established but newly trendy ones like Foursquare or Diplomático, emphasize craftsmanship and authenticity over caricatures, and are successfully piquing millennials’ and Gen Z’s interest. With major spirit companies investing in rum (e.g. Brown‑Forman’s 2023 acquisition of Diplomático to enter the super-premium rum segment), it’s clear that rum is being viewed as the “next big thing” in spirits by some industry leaders.

Looking ahead into 2026, the global outlook for rum is one of cautious optimism. The consensus is that rum will continue to grow in volume and value, but the mix will tilt toward higher-end segments. The biggest opportunities lie in premiumization - especially for dark, aged, and high-quality spiced rums - while capturing younger audiences through ready-to-drink innovations and even no/low-alcohol alternatives. In other words, growth will be driven less by selling more rum to the same consumers, and more by selling better rum and new rum-based experiences to an expanding consumer base. If the industry can address its structural challenges (like fragmented regulations and rum’s lingering reputation in some quarters as a cheap mixer), experts believe rum’s potential in 2026 and beyond could begin to rival the momentum seen in tequila or single-malt whisky.

Regional Highlights: US, UK & Europe, Asia-Pacific

While rum is a global spirit, each region has its own market character and 2025 performance story. Here we highlight three key regions - the United States, Europe (with a spotlight on the UK), and Asia-Pacific - to see how rum trends are playing out around the world.

United States: A Stubborn Slowdown

In the United States, the rum market in 2025 was challenged by stagnation, even as other spirits categories boomed. For the first time in decades, overall spirits volume in the US fell slightly in 2023, and rum was among the categories that struggled to gain momentum. Industry observers note that U.S. rum sales have been flat or in slight decline, especially compared to the red-hot growth of tequila/mezcal and the continued strength of whiskey. By 2024, rum volumes in the US were around 21 million 9-liter cases sold (roughly on par with previous years) - a substantial market, but one that isn’t expanding much. Part of the issue is fierce competition: American whiskeys and agave spirits (tequila) are currently the darlings of the U.S. market, capturing much of the excitement and premium spending. Rum, in comparison, has struggled to shed its image as a fun-but-unsophisticated party spirit.

A closer look reveals structural factors holding rum back in the U.S. The market is still heavily skewed toward low-priced and flavored rums, which make up an estimated 42-43% of U.S. rum volume. Top-selling brands like Bacardi and Captain Morgan move huge quantities, but largely in the form of inexpensive white rum for mixing, or sweet spiced and flavored variants aimed at casual drinkers. This dominance of the value segment has hindered the trade-up to premium rums. Fewer new rum brands have emerged in the U.S. relative to whiskey or gin, and consumer “rum education” remains limited, leading to less enthusiasm in the category. The result is a bit of a stalemate: many American consumers stick with what they know (white rum for their Rum & Coke, spiced rum for a simple punch), while the more adventurous spirits drinkers have been exploring bourbon, rye, tequila, and others.

Economic pressures in 2025 also played a role. High inflation and tighter wallets meant U.S. consumers were careful with discretionary spending, and some opted for cheaper drink options or drank out less frequently. In such an environment, mainstream “party rums” faced heightened price sensitivity - a $5 difference in bottle price can sway a purchase. There is a silver lining: some mid-tier standard rums actually saw a boost as consumers traded down from ultra-budget to mid-shelf, seeking a balance of quality and value. However, the super-premium tier (high-end sipping rums $50 and up) remains a niche in the U.S. and may struggle to expand unless brands create very strong narratives to justify the cost. A few positive signs include the introduction of new brands with celebrity backers (e.g. singer Ciara’s partnership with Ten To One rum) and innovative products like rum-based ready-to-drink beverages hitting the U.S. market. These efforts aim to energize the category and attract younger consumers. For instance, Ten To One - a premium rum brand - has been actively using on-premise promotions and influencer tie-ins to reposition rum as a versatile upscale spirit in urban U.S. markets.

Going into 2026, the U.S. rum market’s challenge is to break out of its holding pattern. Industry leaders believe education and premiumization are key: telling the story of rum’s heritage, promoting cocktails beyond the basic Rum-and-Coke, and highlighting high-quality dark and aged rums. There is also a push for greater transparency (such as labeling real ingredients or lack of additives) to build trust with enthusiasts. If rum can better differentiate itself - for example, positioning certain rums as the “bourbon of the tropics” or tapping into tiki/Latin cocktail trends - it may start to claw back some of the market share lost to whiskey and agave. As of 2026, however, the U.S. remains a cautious market for rum, where innovation and marketing will need to work hard to overcome entrenched competition and perceptions.

United Kingdom & Europe: Premiumization and Cocktail Culture Fuel Growth

Across the Atlantic, Europe - and the UK in particular - has become a hotbed of rum enthusiasm. In the UK, rum’s momentum in 2025 was noteworthy: on-trade rum sales (bars, restaurants) surpassed £1 billion for the first time, even overtaking whisky sales in pubs and bars. This is a remarkable milestone that underscores how mainstream rum has become in British drinking culture. Dark rums led the charge in the UK, posting around +5% growth in 2023, outpacing golden and white rums. Much of this growth was fueled by the ongoing craze for spiced rum and flavored variants among younger consumers. Spiced rums - from big brands to craft entries - have been extremely popular in the UK and parts of Europe, appreciated for their mixability and sweet spice notes. The result: the UK rum category is premiumizing and diversifying at a rapid clip.

Importantly, the UK’s younger demographics are driving this rum renaissance. Consumers in their 20s and 30s are seeking experiences and brands that align with music, art, and local culture. For example, rum brands have partnered with festivals and events - such as Bounty Rum’s presence at the Notting Hill Carnival, a major cultural festival in London - to tap into the vibrant street party scene. These experiential marketing efforts have paid off in making rum “cool” again. The UK has also proven quite open to new brand entries on the premium end; as noted, a brand like Ten To One (founded in the US) found receptive audiences in Britain through strong on-premise programs and local influencer partnerships. The message is clear: British consumers are willing to try new rums, especially if they come with a story, a celebrity endorsement, or a unique twist, and if they are visible in trendy bars.

On the European continent, parallel trends are visible. Western Europe is experiencing a wave of rum premiumization: countries like France, Germany, and Italy reported gains in the super-premium-and-above tier, often driven by brand-led education that encourages sipping rum neat or on ice like a fine whisky. In Germany, for instance, consumers have shown growing interest in unique flavor profiles and authentic craftsmanship in rum, pushing brands to innovate with new cask finishes and small-batch releases. France - with its historical ties to rum-producing islands - has a connoisseur segment for agricole and aged rums that continues to expand. Throughout Europe, cocktail culture has been a major tailwind for rum: classic rum cocktails (Mojitos, Daiquiris, Piña Coladas) regained popularity as bars fully reopened, and a new generation of mixologists incorporated premium rums into inventive craft cocktails. This on-trade trend boosts consumer awareness of high-quality rums and encourages at-home experimentation as well.

One striking feature in Europe is the enduring love for spiced and flavored rums. Europe is the strongest market for spiced rum globally. From classic spiced rums to new flavor infusions (like pineapple, coconut, or coffee rums), European drinkers enjoy the approachable sweetness and versatility of these products. Some research projects the global spiced rum segment to reach nearly $10 billion by 2030 (up from ~$7 billion in 2024), and a significant portion of that demand emanates from European markets. Notably, many European consumers no longer view flavored rums as “inferior” - brands have elevated the quality, offering complex spiced expressions alongside their aged portfolios. For example, a distiller might release a premium spiced rum with exotic botanicals or a high-proof overproof spiced rum for craft cocktail use, targeting both adventurous newcomers and seasoned rum sippers looking for something different.

Europe also benefits from a somewhat more structured regulatory environment for rum compared to the U.S., which helps with consumer trust (more on this in a later section). The European Union’s definition of rum requires it to be distilled from sugarcane products and generally prohibits undisclosed additives beyond certain limits. This means when European consumers buy a bottle labeled “rum,” they can be more confident in what they’re getting, especially in premium categories. Such clarity has likely helped the premium sector: brands that play by the rules (no added sugar/color in “pure” rum) use it as a selling point to the growing geeky fan base in Europe that cares about authenticity.

Heading into 2026, Europe (and the UK at its forefront) seems poised to continue as a growth engine for the rum category. Many industry predictions place Europe as the fastest-growing region for rum in the second half of this decade. New local rum distilleries in places like the UK, Spain, and Scandinavia are popping up, further enriching the market with “European-made” rums and urban craft experiments. The combination of heritage (demand for Caribbean imports and historical brands) and innovation (local craft, novel flavors) makes Europe a vibrant and competitive rum arena. If current trends hold, European consumers will be enjoying more premium sipping rums, more creative rum cocktails, and a greater variety of rum styles in 2026 than ever before.

Asia-Pacific: High Volume and High Potential

Asia-Pacific is the sleeping giant of the rum world, already accounting for the largest share of global rum consumption and holding immense potential for future growth. In 2025, Asia-Pacific’s rum market was the world’s largest regional market, representing about 40% of global rum sales by value. This is not entirely surprising given the region’s population size and the presence of big rum-consuming countries. For instance, India has long been one of the top rum markets globally (by volume, if not by premium value), with iconic brands and a history of rum consumption in the military and civil society. Brands like McDowell’s No.1 Celebration (an Indian dark rum) and Tanduay (from the Philippines) often rank among the highest-volume rums in the world, thanks to their huge domestic followings. As of 2025, the Indian rum market alone was valued around $2.7 billion and is forecast to grow steadily (~4% CAGR to 2030). The Philippines, Thailand, and Australia are other significant rum markets in Asia-Pacific, each with their own local rum culture (the Philippines’ Tanduay and Europe/Asia-exported Don Papa, Thailand’s full-strength local rums, Australia’s Bundaberg, etc.).

What’s particularly exciting for Asia-Pacific is the emerging trend of premiumization and cocktail culture in its major urban centers. Historically, a lot of rum consumed in Asia has been at the value end - affordable dark rums or locally made cane spirits consumed straight or in simple mixes. But this is changing. As disposable incomes rise and the craft cocktail movement spreads to cities like Mumbai, Shanghai, Bangkok, and Sydney, more consumers are discovering quality rum and rum-based cocktails. An industry outlook noted “emerging markets like Turkey, China, and India hold unexploited potential as more consumers explore cocktails and local rum-based experiences.” For example, in India’s metro areas, cocktail bars are popping up and featuring Mojitos and Mai Tais, introducing a new generation to rum’s versatility. In China, while rum is still a very small niche (baijiu and whiskey dominate), bartenders in cosmopolitan cities like Shanghai are using imported Caribbean rums in tiki drinks and tropical-themed bars, slowly building awareness. Asia’s growing tourism (Southeast Asian beach destinations, for instance) also exposes more people to rum cocktails as part of the travel experience, which can translate into curiosity back home.

Another factor is the push by global spirits companies in Asia. International rum brands are ramping up marketing in Asia-Pacific, seeing fertile ground especially for premium products among the expanding middle class and expatriate communities. Asia is already the largest region for spirits in general, so rum’s relatively small share suggests room to grow. For instance, Diageo and Bacardi have been known to test special releases in travel retail across Asia, and companies are educating trade partners on how to serve rum in more elevated ways. Cocktail competitions and festivals are also taking place in the region (e.g., Singapore or Hong Kong cocktail weeks including rum-centric events), further raising the profile of rum among influencers and bar professionals.

It’s worth noting that Asia-Pacific’s growth isn’t uniform: some markets are mature or even shrinking, while others are booming. Australia and Japan have a small but passionate rum aficionado community, with growing interest in high-end and funky rums (e.g., Jamaican pot still rums) among whisky converts. Meanwhile, Southeast Asia (like Philippines, Thailand, Vietnam) consumes a lot of rum by volume but mostly in inexpensive forms - converting even a fraction of those drinkers to mid-range or premium brands would significantly boost value. And then there’s the wildcard of Asia’s own rum production: countries like India, Thailand, the Philippines, and Japan have local rum distilleries that are stepping up quality and could eventually become players on the export scene (for example, Japan’s Ryukyu Awamori, a rice-based spirit, and some molasses-based “Japanese rums” like Nine Leaves are attracting global interest).

Asia-Pacific is also expected to be the fastest-growing region for no- and low-alcohol spirits, including non-alcoholic rum alternatives (as we’ll discuss later), which could influence traditional rum by offering more entry points for consumers concerned about health. Overall, heading into 2026, Asia-Pacific offers a dual narrative: huge existing volume (keeping the wheels of the global rum industry turning), and huge untapped premium potential. If brands can crack the code of local tastes - for instance, offering rum products tailored to Asian palates or occasions - the region could see rum growth accelerate. With Asia-Pacific economies rebounding and younger generations looking beyond traditional spirits, don’t be surprised if rum experiences a notable uptick here, perhaps even more so than in Western markets, in the coming years.

Consumer & Innovation Trends: Premiumization, Flavours, RTDs & No/Low

Rum’s recent and forecasted growth is as much about qualitative changes - how and what rum people are drinking - as it is about quantitative sales increases. Several consumer trends and innovations are reshaping the category. Key among them are the continued premiumization of rum, a surge in flavor innovation (especially spiced and flavored rums), the explosion of ready-to-drink (RTD) cocktails and the related rise of cocktail culture, and the emergence of no- and low-alcohol alternatives in the rum space. Let’s examine each of these trends in turn.

Premiumization: Rum Goes Upscale

Perhaps the most defining trend in the rum market is premiumization - the shift toward higher-priced, higher-quality products. As noted earlier, premium-and-above rums have been leading growth worldwide. For example, in the premium segment of rum, dark rums are driving the lion’s share of growth: premium (and super-premium) dark rum represented only about 11% of that segment in 2019, but grew to 17% by 2024, far outpacing premium growth in white or flavored rum (which still comprise only ~4% of their segments). This indicates that consumers trading up to premium are particularly choosing dark, aged rums - the types often positioned for sipping or upscale cocktails. Indeed, the premium rum market itself is forecast to expand robustly, from roughly $5.25 billion in 2024 to $8.45 billion by 2033 (a healthy ~5.6% CAGR). In North America and Europe, the buzz around craft and aged rums is at an all-time high, driven by a cohort of spirit enthusiasts aged 25-44 who crave authentic narratives and distinctive production techniques behind their drinks.

So what defines premiumization in rum? It involves both product and storytelling improvements. On the product side, we see more rums with age statements, single-barrel or single-origin releases, cask finishes (e.g. rums finished in sherry, wine, or whiskey barrels), and limited editions like vintage or small-batch bottlings. A great example is Brugal’s ultra-premium “Andrés Brugal Edition 02” launched in 2025 - only 416 bottles, priced around $3,000 each, showcasing rare casks and aimed at collectors. Such offerings, unthinkable a decade ago for rum, underline how far the premium ceiling has risen. On the storytelling side, authenticity and expertise are key. Premium rum brands now emphasize elements like terroir (e.g., a single-island or single-estate rum), unique fermentation and distillation methods, and transparency in production. According to Park Street (a spirits industry firm), producers are distancing themselves from gimmicky branding and instead focusing on production techniques and rich heritage, which “has attracted younger drinkers” and elevated rum’s status. For instance, Barbados’s Foursquare Distillery is lauded for not adding sugar and for its master distiller’s craft approach, which resonates with connoisseurs and has made Foursquare’s limited releases very sought-after.

Critically, education is accompanying premiumization. Brands and importers are investing in consumer education - hosting tastings that compare a $20 rum to a $60 rum, explaining the difference in aging or ingredients, much like has been done for Scotch or bourbon. They are also pushing for transparency to build trust. As one report noted, publishing clear details on aging, sugar additions, and distillation fosters a “trusted brand” aura among premium consumers. Some companies are even adding QR codes on bottles that link to detailed production info (e.g. which farm the molasses came from, fermentation days, etc.) to satisfy the curiosity of spirits geeks. All these efforts aim to reposition rum from a one-dimensional party spirit to a multi-faceted, premium craft spirit. And it’s working - premium rum sales in certain high-end bars and restaurants have significantly outperformed average spirit growth (in one segment of U.S. dining venues, premium rum sales were 42% higher than average, indicating strong demand in quality-focused outlets). As we move into 2026, premiumization is expected to remain the engine of rum market value growth, converting more drinkers to sipping rums, and commanding higher price points that boost revenue even if volumes rise modestly.

Flavour Innovation: Spiced and Beyond

The rum category has embraced flavor experimentation in recent years, leading to a renaissance of spiced and flavored rums. While dark/unflavored rum still holds the dominant market share by sheer volume, the exponential growth in spiced and flavored variants represents a parallel trend brands cannot ignore. Spiced rum, long popular in certain markets, has broken out globally: it was valued around US$7 billion in 2024 and is projected to reach roughly $10 billion by 2030. This is a significant jump for a subcategory once considered a niche - clearly, spiced rum has gone mainstream. In Europe, spiced rums are particularly entrenched, appealing to both entry-level drinkers (who find them smooth and approachable) and to seasoned rum fans looking for something novel in their rotation.

What’s driving this flavor boom? Versatility and mixability are big factors. A good spiced or flavored rum can be sipped neat by those who enjoy a touch of sweetness, but it truly shines in simple mixed drinks - think spiced rum with ginger beer, or coconut rum with pineapple juice. Consumers have learned that flavored rums can enhance cocktails easily, which ties into the broader cocktail culture upswing. Additionally, flavors like vanilla, coconut, mango, pineapple and coffee hit a sweet spot for younger drinkers who have a penchant for sweet and exotic taste profiles. As cocktail culture grows, people understand how different rum flavor profiles (say, a coconut vs. a dark cinnamon spiced rum) can each enhance certain cocktails, from tropical tiki drinks to flavored Mojitos. This has encouraged more exploration of flavored rums rather than viewing them as low-end products.

Another reason is the sheer creativity distillers are now applying. No longer is a “flavored rum” just a basic silver rum with some artificial flavor thrown in. Many brands are experimenting with botanical infusions, exotic spice blends, and innovative aging techniques incorporating various spices or woods. For instance, some craft producers create spiced rums using whole botanicals and barrel-aging the spiced blend to integrate flavors more naturally. Others are playing with flavor combinations like chocolate-orange rum or spiced rums finished in port casks. This kind of creativity is expanding rum’s appeal across a spectrum of taste preferences and redefining consumer expectations of what a flavored spirit can be.

Crucially, the industry is changing the narrative that “flavored = inferior.” Today, flavored no longer means inferior in rum. Some respected distilleries are positioning complex spiced expressions alongside their pure aged rums, essentially saying it’s possible to have a high-quality spiced rum that serious enthusiasts can appreciate. This approach is winning over both adventurous newcomers (who start with a tasty spiced rum and then might graduate to trying the unflavored lineup) and experienced drinkers seeking unique experiences beyond the usual fare.

We can expect flavour innovation to continue in 2026. Some trends to watch: more natural and craft-inspired flavors (e.g., botanical rums with real herbs or fruits), collaboration with other industries (perhaps a rum aged with coffee beans, or a partnership with a chocolate company for a cacao-infused rum), and a focus on authenticity in flavoring (transparently stating what’s used for flavor). Also, as consumers become health-conscious, there may be a tilt toward flavored rums with no added sugars or all-natural ingredients, to appeal to label-scrutinizers. In summary, flavor innovation is broadening rum’s fanbase and giving existing fans new products to explore - an essential part of keeping the category vibrant.

RTDs and Cocktail Culture: Convenience Meets Craft

Another trend turbocharging rum’s popularity is the global cocktail renaissance and its spillover into ready-to-drink (RTD) cocktails. In recent years, cocktails have undergone a renaissance worldwide - both in high-end bars and at home. Rum, with its incredible versatility (it’s the base of countless classics and tropical drinks), is ideally positioned to benefit. As a key ingredient in Mojitos, Daiquiris, Piña Coladas, Mai Tais, Dark ‘n Stormys and more, rum is deeply embedded in cocktail culture. Bartenders praise rum’s adaptability, using it in everything from simple highballs to complex tiki concoctions. This bartender endorsement has a ripple effect: what’s popular with mixologists eventually influences consumer behavior in the broader market. Indeed, industry observers note that as bartenders favor rum for its mixability, it “influences consumer behaviour at home as well as in bars”. During pandemic lockdowns, many consumers learned to make rum cocktails at home; by 2025, that trend evolved into a home bartending revolution, with people continuing to mix their own Daiquiris and rum punches, effectively democratising cocktail culture beyond the bar scene.

Amid this cocktail boom, ready-to-drink cocktails (RTDs) have emerged as a fast-growing category - essentially canning or bottling that craft cocktail experience for convenience. The RTD category is already huge and getting bigger: global RTD sales are forecast to hit $40 billion by 2027 (across 10 key markets). From 2025 to 2027 alone, RTDs are predicted to grow by about +12% in volume, far outpacing the growth of traditional spirits. Rum-based RTDs form an important slice of this pie - think canned Rum & Cola, Mojito in a can, Mai Tai pouches, etc. In 2025 we saw major launches like Captain Morgan & Vita Coco’s coconut water-rum premixed drink, a collaboration bridging a spirits brand and a non-alc beverage brand. Such partnerships highlight how companies are keen to leverage rum’s tropical, fun image in RTD form.

The appeal of RTDs is straightforward: they offer quality + convenience. Modern RTDs aren’t the overly sweet, low-quality malt beverages of yore; many are spirit-based, using real rum and quality mixers, marketed as bar-quality cocktails you can drink anywhere. This trend dovetails with health and lifestyle shifts too. Consumers want convenience, but they also care about what’s in their drink. Successful RTD strategies “think beyond mere convenience to address the full spectrum of modern consumer priorities, such as health, quality, authenticity, and experience.”. For example, newer rum RTDs often tout natural ingredients, no artificial flavors, sometimes even lower calorie counts or lower alcohol content to appeal to the health-conscious. We’re essentially seeing quality cocktails being blended with convenience in a can - a very attractive proposition for someone who wants a quick highball at a picnic or a beach day without mixing ingredients.

Rum stands to gain a lot from this. Why? Because many classic tropical cocktails are rum-based, and those translate well to pre-mixed formats. Additionally, rum’s tropical cachet makes it easy to market these RTDs with imagery of beaches and palm trees - resonating with consumers looking for a little escapism in their drink. Brands are wise to ensure their RTDs carry real “rum credentials”. There’s a subtle but important distinction between spirit-based RTDs and cheaper malt-based “cocktail-flavored” beverages. Educating consumers that a canned “rum punch” actually contains real rum (not just a flavor) is part of premiumizing the RTD segment. As one strategy document suggested, rum brands should position their RTDs as authentic and “label them as ‘spirit-based’ cocktails rather than malt-based imitations.”. We can expect more innovation here in 2026: possibly new rum RTD flavors (beyond the basics, maybe things like a canned Hurricane or Rum Old Fashioned), collaborations (rum brands partnering with soda or juice brands for unique mixes), and even craft RTDs from boutique rum distillers. All of this will extend rum’s reach to occasions where mixing a cocktail isn’t practical, thus enlarging rum’s footprint in the overall drinks market.

No/Low Alcohol Alternatives: Sober Curious Meets Rum

A few years ago, the idea of non-alcoholic rum might have sounded like an oxymoron. But as we approach 2026, no- and low-alcohol (“No/Low”) beverages have firmly entered the mainstream - and even the rum category is seeing alcohol-free or low-ABV alternatives emerge. What’s driving this is a significant cultural shift: consumers (especially Gen Z and younger millennials) are increasingly health-conscious and moderation-minded. Globally, the no/low alcohol segment is expected to grow about +4% in volume CAGR through 2028, outpacing the traditional alcohol sector’s growth. By value, the no/low category reached about $13 billion globally and is on track to comprise nearly 4% of total alcohol volume by 2027. In other words, it’s moved from niche to a noticeable chunk of the market.

For rum, this trend materializes in a couple of ways. Firstly, there are non-alcoholic “spirit” alternatives that mimic rum’s flavor profile. These are often distilled botanicals or flavored beverages that have the aroma and taste reminiscent of rum, but 0% ABV. According to a recent market report, the global non-alcoholic rum alternatives market is “projected to grow from $1.17 billion in 2024 to $1.94 billion by 2029” (a CAGR of 10.5%). That’s a substantial growth, indicating strong demand for rum-like flavors without the alcohol. Key players in this space - such as Caleño (UK-based) and Ritual Zero Proof (US, recently acquired by Diageo) - offer products like alcohol-free spiced “rum” or coconut “rum” alternatives. These products are often used in mocktails or enjoyed with mixers, letting people have a “rum and cola” experience minus the booze.

Secondly, even traditional rum brands are paying attention to low-ABV options. Some have introduced lower-proof versions or are actively promoting rum-based drinks with less alcohol. For example, a rum spritz or a sessionable cocktail that uses less rum and more sparkling water, etc., to cater to moderation trends. In bars, it’s now common to see a section of the menu for low-alcohol or zero-proof cocktails. Many top bars treat zero-proof cocktails with the same craft care as regular ones, using premium alcohol-free spirits and fresh ingredients. So a guest can have a thoughtfully made faux Mojito or alcohol-free Punch that still uses a rum alternative for flavor. This means someone who loves rum flavor doesn’t have to consume alcohol every time to enjoy it - a major shift from the all-or-nothing choice of the past.

The reasons behind the No/Low trend’s momentum are well documented. Health and wellness is a big one: consumers are more mindful of their alcohol intake for physical and mental health. Many practice “Dry January” or moderation techniques like “zebra striping” (alternating alcoholic and non-alcoholic drinks on a night out). Younger generations in particular are drinking less on average; about 40% of Gen Z adults have never tried alcohol at all. This doesn’t mean they don’t want interesting beverages - they do, but without the alcohol. The industry has responded by making sure alcohol-free doesn’t mean flavor-free or experience-free. The best alcohol-free spirits, including rum alternatives, try to mimic the warmth or spice of alcohol so that a mocktail still feels “adult” and special. For instance, Ritual Zero Proof’s rum alternative is noted for being a dark rum replica with spice notes, aimed at giving a satisfying substitute for rum in a drink.

From a rum market perspective, No/Low is incremental opportunity: studies show these products largely bring in new consumption occasions rather than cannibalize regular alcohol sales. A rum drinker might switch to a non-alcoholic rum cocktail on a weeknight when they don’t want the buzz, rather than not drink anything at all - that’s a net gain for the industry’s sales. Big spirits companies have noticed; the fact that Diageo (which owns Captain Morgan rum among other brands) purchased Ritual Zero Proof in 2024 shows strategic intent to cover all bases. We can expect more partnerships and product launches bridging rum with the wellness space. Imagine, perhaps, a major rum brand launching its own non-alcoholic spiced rum mixer, or more low-sugar, low-proof canned cocktails.

In 2026, the presence of rum in the low/no segment will likely grow, not shrink. While it will remain a relatively small slice of the rum world in pure financial terms, it plays an outsized role in shaping perceptions and keeping rum relevant for a new wave of consumers who demand choices. The best part is, it reinforces rum’s versatility: whether you want a stiff Navy-strength rum or a zero-proof tropical cocktail, the flavor of rum can be part of your experience.

Sustainability, Authenticity & Regulatory Landscape

Beyond product trends, the rum industry is also undergoing important shifts in how rum is produced, marketed, and governed. Sustainability and ethical practices are increasingly vital as consumers (and stakeholders) look for environmentally and socially responsible brands. Authenticity and transparency have become watchwords, especially in the premium segment, as producers strive to build trust and differentiate genuine quality from gimmicks. Meanwhile, the regulatory landscape for rum - historically looser and less standardized than for spirits like Scotch or tequila - is coming under scrutiny, with efforts (and some struggles) to establish clearer rules. These three areas are interconnected: authenticity often ties into regulation (e.g., defining what “real rum” is), and sustainability often dovetails with authenticity (e.g., being true to local communities and ingredients). Let’s break down each aspect:

Sustainability: Green Horizons for Rum

From cane field to bottle, rum production has a significant environmental and social footprint. In 2026, more brands are recognizing that adopting sustainable and ethical practices is not just good for the planet, but also a smart business move as consumers increasingly demand it. Modern consumers - especially younger Millennials and Gen Z - “don’t simply focus on the drink in their glass; they are interested in the journey it took to get there.” In other words, how was the rum made? Were the ingredients farmed sustainably? Were the workers treated fairly? What’s the carbon footprint? These questions are now common, and savvy rum companies are actively providing answers.

One concrete development is the rise of certifications and standards in rum production. For instance, an increasing number of distilleries are pursuing certifications like Bonsucro (sustainable sugarcane certification), Fair Trade for sugarcane molasses, and even organic certifications. E&A Scheer, a major rum supplier, notes that they maintain Bonsucro, Fairtrade, and Organic certifications, and this is a broader trend - third-party seals that lend credibility to sustainability claims. Such certifications ensure practices like reducing water usage, ensuring fair labor conditions on cane farms, and minimizing chemical inputs. They also address a historical challenge: sugarcane agriculture has sometimes been associated with deforestation or labor exploitation; these certifications aim to flip that narrative toward regeneration and fairness.

Distilleries are also taking steps to reduce their environmental impact across the value chain. This might include: sourcing local or traceable cane to reduce transport emissions, investing in renewable energy for distillation (some Caribbean distilleries use bagasse - the fiber waste from crushed cane - as biofuel to power operations), capturing CO2 from fermentation, treating wastewater so it doesn’t pollute rivers, and using recyclable or lightweight packaging to cut down waste. For example, some rum brands have switched to recycled glass bottles or eliminated plastic from their packaging. Others are working on reducing the angel’s share in aging warehouses (high humidity warehouses can reduce evaporative losses, indirectly saving resources). These moves are sometimes costly upfront, but many brands see them as necessary investments in the future.

An important point is that sustainability in rum is no longer just a niche marketing angle - it’s increasingly expected. Environmentally aware drinkers actively seek out brands that align with their values. This means that brands who embrace sustainability can build a lasting competitive advantage and brand loyalty. As the E&A Scheer insight puts it, “Sustainability isn’t a cost. It’s a competitive advantage.” Brands that clearly communicate their eco-credentials often attract those consumers who might pay a bit more for a product that aligns with their principles. We’ve seen some rum brands highlight, for example, “carbon neutral rum” or partnerships with reforestation projects (like planting trees in the tropics) as part of their story. Not only does this attract environmentally conscious consumers, it also helps “stand out in an increasingly crowded marketplace” by giving the brand a distinct ethos.

Social sustainability is just as crucial: ensuring local communities benefit. Many rums are produced in developing regions (Caribbean, Latin America, parts of Asia). Companies are now more frequently touting how they support local communities, whether through providing good jobs, supporting local schools, or preserving local heritage (authentic production methods, GI protections, etc.).

In summary, 2026 will see sustainability as a standard part of the rum conversation, not an afterthought. We can anticipate more brands proudly advertising their green initiatives and more collaborations across the industry to raise the bar (for example, sharing best practices on wastewater treatment or cane farming improvements). The ones that lag on this front risk being called out by consumers or advocacy groups. In rum, as in other categories, doing good is increasingly linked with doing well in business.

Authenticity & Transparency: Telling the True Story

As rum premiumizes, authenticity has become the currency of credibility. Discerning consumers want to know that the bottle they bought has a real story and integrity behind it, not just marketing smoke and mirrors. In the past, rum marketing often leaned on fabricated legends or cartoonish characters; today, it’s shifting to focus on provenance, craftsmanship, and transparency.

Authenticity can mean highlighting heritage - e.g., a rum brand emphasizing it’s made in the Caribbean island where rum originated, or using centuries-old techniques. It can also mean being honest about production - for example, disclosing if sugar or flavoring has been added, or explaining that a “12-year rum” is genuinely aged 12 years (not a blend with a drop of 12-year and a lot of younger spirit, a practice that some less scrupulous brands used in the past). The push for authenticity is partly a response to rum historically lacking the tight regulations of, say, Scotch whisky. Rum has had a “Wild West” reputation in labeling, which savvy consumers became aware of - e.g., some rums quietly added sugar or coloring, or sourced rum from elsewhere than the label implied. This has led to a bit of a trust gap at the high end.

Brands are working to close that gap through transparency initiatives. For instance, some producers now list the dosage (sugar added) on their websites or labels, voluntarily, even though not required, to show they have nothing to hide. Others are very clear about aging (like stating “minimum aged X years” to mimic whisky’s approach). The use of clarity in labeling is often mentioned as a must-do; as one analysis recommended, “Transparent labeling that details cask origin, sugar content, and production technique” can foster trust and educate consumers. Indeed, such transparency could become a de facto expectation among premium rums - much like an ingredient list in food.

One interesting development on the authenticity front is the creation of geographical indications (GIs) and appellations for rum. Just as Cognac must come from Cognac, France, and abide by certain rules, some rum-producing regions are formalizing their standards. For example, Jamaica has a GI for “Jamaican Rum” which sets rules (like prohibiting artificial flavors and requiring local aging) to protect the integrity of Jamaican rum. However, as recent events show, this can be contentious; in 2024-2025, Jamaican distilleries clashed over GI rules (particularly about whether rum can be exported in bulk and aged overseas). An interim court ruling in Jamaica even put a hold on implementing stricter GI rules, illustrating the tension between authenticity and business flexibility. Despite the bumps, these GI discussions underscore the desire among producers to define what makes their rum special and genuine. We also have longstanding examples like Martinique’s AOC for Rhum Agricole (a very strict French appellation) which has helped market agricole rhum as a premium, terroir-driven product.

Beyond regulations, authenticity is communicated through storytelling. Brands now share detailed backstories: the history of the distillery, the master blender’s philosophy, the community around the rum. This resonates particularly with premium consumers who often are seeking an experience, not just a liquid. As mentioned earlier, producers like Brugal, Diplomático, or smaller craft distillers highlight their unique production and history, which has successfully “attracted younger drinkers” by giving them something real to latch onto. Authenticity also means aligning endorsements or partnerships that make sense - e.g., if a celebrity is involved, making sure they genuinely love the product or represent its values, otherwise it feels hollow and consumers sense that.

In 2026, expect authenticity to be a key selling point in rum marketing and product development. We may see more rums released with full disclosure information pamphlets (some independent bottlers already do this, listing distillation date, barrel type, additives, etc.). Additionally, communities of rum aficionados (often online) continue to scrutinize products - a practice that effectively holds brands accountable. A brand that markets a “premium aged rum” that’s been sweetened heavily might face criticism in enthusiast forums, which pressures everyone to be more genuine. In short, authenticity is both a consumer demand and an industry strategy: it helps rum stand out in a crowded market by offering something real, and it builds the kind of trust that leads to long-term brand loyalty.

Regulatory Landscape: Seeking Standards Amid Complexity

One of rum’s historical quirks is the lack of a unified global standard for production and labeling. Unlike categories such as Scotch whisky (which has strict laws recognized worldwide) or tequila (protected by denomination of origin), rum’s definitions can vary by country. This regulatory patchwork has often been cited as a hurdle for the category’s premium development. In 2025, the theme of “lack of unified regulations” came up repeatedly in industry reports, emphasizing that the absence of standardized rules “undermines consumer trust in premium rum.”

What exactly are the regulatory inconsistencies? A few examples: The European Union defines rum as a spirit from fermented cane products distilled below 96% ABV, aged at least if flavor is derived from wood (some rum must be aged minimum 1 year in the EU definition), and critically, if more than 20 grams of sugar per liter are added, it cannot be called rum (it would be a “spirit drink” or liqueur). The United States, on the other hand, defines rum simply as a spirit distilled from cane at less than 95% ABV, but it allows coloring/flavoring up to 2.5% without disqualifying it as rum, and has separate classifications for “flavored rum” (which can have more additives). So a bottle that must be labeled “spiced spirit drink” in Europe might just be “Spiced Rum” in the US. There are also variations in minimum ABV: EU requires at least 37.5% ABV for rum, the US requires 40%. These differences mean a rum producer often has to navigate different formulations or labels for different markets, which is a headache and can confuse consumers globally.

Additionally, some countries have their own laws: e.g., Mexico passed a regulation defining rum in 2020 for their domestic market; France has AOC for Martinique rum as mentioned; Caribbean community (CARICOM) has regional standards (but not all Caribbean rums follow one standard). The net effect: ambiguity in labeling (like sugar addition, true age statements, distillation method transparency) can erode trust. For premium rums, a buyer might wonder, “Is this really pure rum or has something been added?” - a question they wouldn’t have to consider with a regulated Scotch or bourbon. This uncertainty is what the calls for unified regulation aim to eliminate.

There are efforts underway to tighten standards. Aside from regional GIs, organizations like the West Indies Rum & Spirits Producers Association (WIRSPA) have a voluntary scheme (the Authentic Caribbean Rum (ACR) mark) which certifies rums that adhere to certain production criteria. However, this is not legally binding everywhere. Some enthusiast groups and independent bottlers champion what’s called the Gargano Classification (categorizing rum by production method - pure single rum, traditional rum, etc.) as an educational tool, though it’s not law.

The industry is aware that to truly compete with whiskey or cognac at the high end, it helps to have clearly communicated standards. We might see movement in 2026 towards more consensus on labeling. For example, perhaps more countries adopting the EU-like stance that added sugar must be disclosed or limited. Or maybe a global code of practice for rum producers. The issue, of course, is that producers who benefit from looser rules may resist stricter ones (as seen in the Jamaican GI dispute where some wanted to continue aging in Europe because it’s cheaper/cooler climate, while others wanted to ban that for authenticity).

From a market perspective, this regulatory complexity is a challenge on multiple fronts: it complicates international trade (different approvals needed), it can confuse or mislead consumers, and it allows subpar products to sometimes masquerade as something they’re not, undercutting those who play by stricter rules. One solution aside from official regulation is what we discussed under authenticity - producers voluntarily adopting higher standards and educating consumers about them. Indeed, some reports suggest rum brands partner with independent associations or groups that advocate clearer classifications. By uniting and perhaps self-regulating to an extent, rum producers can push the whole category’s reputation upward.

In conclusion, the regulatory landscape in 2026 is still in flux for rum. It’s a point of pain but also potentially a point of progress. The optimistic view is that as rum gains prominence, there will be more impetus to sort out global standards (perhaps via international bodies or trade agreements). If successful, that could dramatically enhance rum’s image and ease of marketability globally. Until then, consumers will rely on trusted brands and third-party endorsements (like awards, reviews, or certification marks) to navigate rum’s diverse offerings. For the rum industry, the message is clear: speaking with a unified voice on quality standards will make it easier to sell the rum story to regulators and consumers alike.

Marketing & Engagement Strategies: Festivals, Collaborations & Digital

With so many changes in products and consumer preferences, rum brands have also been evolving how they market and engage with consumers. In 2026, successful rum marketing is a multifaceted mix of live experiences, creative partnerships, and savvy digital outreach. We highlight a few key avenues: festivals and events that immerse consumers in rum culture, collaborations (from celebrity ambassadors to cross-brand partnerships) that extend rum’s reach, and all things digital and experiential - including social media, e-commerce, and interactive campaigns that bring the rum story directly to the consumer.

Festivals & Events: Bringing Rum to the People

One of the most vibrant ways to market rum is by creating real-world experiences where consumers can taste, celebrate, and learn about the spirit. Rum festivals have proliferated worldwide, from boutique tasting events to massive carnival-like celebrations. These events have become crucial for brands to generate buzz and loyalty. For example, the UK hosts the long-running UK RumFest in London, drawing rum enthusiasts to sample dozens of brands each year. The Caribbean, naturally, has events like the Barbados Food and Rum Festival, and the U.S. has city-based rum festivals (Miami Rum Congress, California Rum Fest, Texas Rum Festival, etc.). At these gatherings, brands set up booths to provide samples (often of new or limited products), conduct masterclasses or seminars, and engage one-on-one with consumers. The value here is education and immersion - a consumer might discover a new favorite rum or finally understand the difference between Jamaican pot still rum and Cuban-style rum by talking to brand reps or attending a workshop.

Beyond dedicated rum festivals, brands are also tapping into broader cultural events. A standout example mentioned earlier is how rum brands piggyback on the Notting Hill Carnival in London - Europe’s biggest street carnival, rooted in Caribbean culture. Bounty Rum’s activation at the carnival is a case in point: by aligning with music and celebration that match rum’s fun image, they ingratiate the brand into culturally significant moments. In the U.S., rum companies sponsor or appear at regional rum and tiki events (like the Polynesian-themed Tiki Oasis gatherings) and also at general spirits events or cocktail weeks. There’s also a move to localize events: as one strategy suggests, “attend or sponsor regional rum fests (e.g., Texas Rum Fest, Florida rum gatherings) to excite local consumers”. This implies that instead of just national advertising, rum marketers are hitting the road to build grassroots support.

Engagement through events often yields intangibles that traditional ads can’t: a sense of community and memory. If someone has a great time at a rum festival, trying ten rums and dancing to reggae, they will associate rum with positive, maybe even nostalgic feelings. It’s similar to how whisky distilleries bank on distillery tours - experiences cement loyalty. For rum, which is trying to cultivate a more premium, connoisseur image while keeping its fun side, experiential marketing is key. We’ll likely see more thematic events (e.g., a pop-up “Rum Beach” bar in an urban winter setting to give tropical escape vibes, or cocktail competitions that double as consumer parties).

Collaborations & Partnerships: Strength in Numbers

In marketing, partnerships can amplify a message by combining fan bases or lending credibility. The rum world has seen a number of interesting collaborations. One type is celebrity partnerships. We touched on a few: rapper Lil Wayne’s endorsement of Bumbu Rum, or singer Ciara investing in Ten To One Rum. These tie-ups can spark consumer curiosity, especially if the celebrity has a genuine tie to the product (Lil Wayne, for instance, integrated Bumbu into his music videos and persona). However, as experts caution, “ensure authenticity - a forced celebrity tie-in can backfire if it doesn’t align with the brand’s heritage or story.” In 2026, the playbook for celeb partnerships is to make them meaningful: perhaps a celebrity who actually has cultural roots or true passion for rum, rather than just a paycheck endorsement. We might also see micro-influencers (like famous bartenders or social media cocktail personalities) be involved in creating special rum releases or campaigns, which can carry a lot of weight among enthusiasts.

Another collaboration angle is co-branding between companies. A notable example is the RTD we discussed: Captain Morgan (rum) partnering with Vita Coco (coconut water) to create an RTD. This merges two brand strengths - one in spirits, one in non-alc - to create a product neither could have done as credibly alone. We could envision similar cross-overs: maybe a rum brand partnering with a coffee company to make a canned rum coffee cocktail, or with a soda brand to market a high-end Rum & Cola set. These partnerships usually come with joint marketing budgets and combined distribution channels, meaning rum can reach new audiences (like Vita Coco’s health-oriented customer base, in the example, who might not be typical rum drinkers).

Collaboration with the on-trade (bars/restaurants) is also crucial. Many rum brands in 2025-26 have programs to work closely with bartenders - effectively turning them into brand ambassadors. Some host global cocktail competitions (e.g., the Bacardi Legacy competition, or plantation rum’s competitions) where bartenders create new cocktails with their rum, driving innovation and word-of-mouth among the trade. Others do private label partnerships with hospitality venues: as E&A Scheer noted, more hotels, restaurants and retailers are developing their own unique rums as proprietary products. This trend has seen private label rum (exclusive bottlings for a certain bar or store) grow to about 9% of the market. For example, a luxury hotel might commission a special cask of rum bottled just for them to offer to VIP guests - it adds exclusivity for the venue and gives the rum producer a prestige placement. This kind of bespoke partnership is a win-win: the venue gets a unique offering, and the rum brand secures a loyal outlet and association with premium experiences. It’s likely we’ll see more creative private labels, like limited-edition rums for cruise lines, airline first-class lounges, or high-end nightclubs.

Local cultural collaborations also play a role in making rum relevant. For instance, brands tie in with local artists for label designs or events (as hinted for UK, partnering with local artists at festivals). In the U.S., some craft distillers partner with breweries or wineries to do barrel swaps (rum finished in ex-wine barrels and vice versa), which cross-pollinates fan bases.

In essence, collaboration marketing for rum extends the reach of the brand beyond the usual channels. It’s about tapping into existing communities - whether that’s fans of a celebrity, patrons of a certain bar, or aficionados of a flavor - and bringing them into the rum world through a trusted bridge.

Digital & Experiential Marketing: Storytelling in the New Age

Last but not least, rum brands are embracing the power of digital media and interactive experiences to engage consumers, especially as younger generations are digital natives. A strong digital presence is now standard: nearly every brand has active Instagram, Facebook, and increasingly TikTok profiles, where they share cocktail recipes, highlight brand stories, and collaborate with influencers. User-generated content is big in the cocktail space - people love sharing their own Mai Tai creation or a photo of that cool rum bottle they bought - and brands often reshare these, fostering a community feel.

One notable digital trend is the expansion of online alcohol retail. Laws have liberalized in many places, and by 2025 online alcohol sales were set for strong growth (IWSR had predicted certain markets’ online alcohol sales to triple from early 2020s levels). Rum brands benefit by being able to sell or market directly to consumers through e-commerce. This is particularly great for niche or premium rums that might not get large physical distribution - enthusiasts can find them online. It also allows for more storytelling at point of sale: a brand’s website or a specialized retailer can include rich descriptions, videos from the distillery, etc., to educate the buyer (whereas on a store shelf, a bottle only has a label to do that). The forecasted expansion of online alcohol retail channels is indeed cited as a trend that will drive rum growth. In 2026, we’ll likely see more brands offering limited releases sold online only (creating a buzz and scarcity effect), and leveraging big online spirits marketplaces to reach international audiences.

Moreover, brands are integrating technology into the consumer experience. Earlier, we mentioned QR codes on bottles linking to detailed info - that’s a simple but effective digital handshake from bottle to smartphone. Some brands have gone further with augmented reality (AR) labels or apps (for example, a few years back a whisky brand had an AR app that brought their label to life with a story when viewed through a phone; rum could easily do similar). Digital campaigns that tie into cultural moments - like Instagram live cocktail classes during Dry January using their non-alc spirit, or a YouTube series on tiki history sponsored by a rum brand - are tools to both educate and create brand content.

Crucially, digital also enables two-way interaction. Brands can get feedback, conduct polls (which new flavor should we launch?), and build communities (Facebook groups or brand-run forums). The more a consumer feels connected to a brand’s world, the more likely they are to stick around. A term often used is experiential marketing, which doesn’t always mean in-person - it means giving the consumer an experience of the brand. This could be a virtual rum tasting hosted over Zoom (something that became popular during the pandemic and still continues for geographically dispersed audiences), or an interactive cocktail-making game online.

One trend that merges physical and digital is the concept of the omni-channel experience - for instance, a consumer at a bar tries a cocktail with a certain rum, scans a code to get a discount to buy that rum online later, then follows the brand on Instagram for more recipes. Brands orchestrating these touches ensure that a curious consumer can easily go from discovery to education to purchase, seamlessly.

Finally, experiential also means unique physical experiences. We covered festivals, but brands have also opened branded venues (like Havana Club’s Casa in Cuba for tours, or pop-up beach bars in cities). These are marketing investments in giving consumers a slice of the rum lifestyle. In 2026 we might see more brand homes or sponsored bars that serve as an advertisement you can walk into - such as a Planter’s Rum rooftop bar for summer in a big city, etc.

In summary, the marketing playbook for rum in 2026 is rich and diverse. Gone are the days when a few magazine ads and a poster of a pirate could do the trick. Now it’s about immersive storytelling - whether through a carnival dance, a collab with someone you admire, or a captivating Instagram story - all aimed at making consumers not just buyers, but fans of rum. And if rum can keep capturing hearts and minds through these creative strategies, it will continue converting more people to the cause of enjoying rum in its many splendid forms.

Challenges: Competition, Economic Pressures & Regulatory Complexity

No discussion of the rum market’s future is complete without acknowledging the challenges and headwinds the category faces. While the trends are promising, rum brands must navigate a competitive and economic minefield. Here, we consider three broad challenges: intensifying competition (both from within the spirits sector and from new substitutes), economic pressures that can alter consumer behavior, and the regulatory complexities that we touched on earlier which can complicate rum’s progress. How the industry addresses these challenges will, in large part, determine whether the projected “rum boom” truly materializes or stalls.

Competition from Other Beverages

In the battle of spirits, rum does not fight alone. It jostles for consumer preference alongside giants like whiskey, vodka, and tequila. In recent years, rum has found itself somewhat in the shadow of a tequila and whiskey surge. For instance, in the US, tequila and mezcal combined overtook rum in sales, growing at double-digit rates as Millennials and Gen Z showed a huge affinity for agave spirits (a trend partly fueled by celebrity tequila brands and the perception of tequila as a “pure” spirit). American whiskeys and single malts also continue to ride high on decades of collector enthusiasm. This means rum is often the category fighting for attention - a common scenario in bars is a patron deciding between a trendy tequila cocktail or a whiskey neat or maybe a rum drink; often rum might be the third or fourth thought.

Additionally, within rum itself, competition is heating up as new brands and expressions flood the market. While this is great for consumers, it means established players must work harder to maintain loyalty. In some markets, local craft distilleries produce rums that compete with imported brands - for example, a UK consumer might opt for a British-made craft spiced rum over Captain Morgan, just for novelty or local pride. Similarly, Indian or Filipino consumers might stick to beloved local brands which are priced very competitively, making it hard for international premium brands to break in.

Rum also faces competition from adjacent categories, like ready-to-drink beverages and flavored malt beverages for the same “occasion”. A casual beer or a hard seltzer might be chosen over a rum cocktail by calorie-conscious or convenience-seeking consumers. Hard seltzers exploded in the US, for example, as a low-cal alternative to cocktails - and though their growth has tempered, they remain a factor. Non-alcoholic options, too, ironically compete with rum in some contexts; a health-conscious person might choose a non-alcoholic cocktail one night, meaning that’s one less rum drink consumed (even if the flavor might be rum-like).

To combat these pressures, the rum industry is leaning on what makes rum unique: its wide flavor diversity and historical mystique. Unlike vodka (flavor-neutral) or even tequila (which, while complex, has a narrower profile range), rum can be grassy, funky, sweet, dry, heavy, light - the spectrum is vast. Educating consumers that rum can be as serious as whiskey, as versatile as vodka, and as exotic as tequila is an ongoing challenge but also the path to carving a distinct identity. Success stories exist - consider how tequila repositioned itself (with help from celebrity backing and emphasis on 100% agave) from party shots to a premium sip-worthy spirit. Rum is attempting a similar journey. If it succeeds, rum can stand not just as “another brown spirit” but as a category people actively collect and explore, thereby standing strong against competition. It may also mean positioning rum in cocktails that traditionally belonged to other spirits - e.g., promoting a Rum Old Fashioned or Rum Negroni to lure whiskey or gin drinkers into trying rum in formats they love.

Economic Pressures and Uncertain Markets

The global economic climate directly impacts spirits consumption. Rum, spanning from cheap to luxury price points, feels these impacts in different ways across segments. In 2025, inflation was a significant issue in many regions (the ripple of pandemic stimulus, supply chain disruptions, war in Ukraine affecting grain and energy prices, etc.). High inflation and cost of living increases dampened discretionary spending in markets like Western Europe and parts of North America. When consumers’ budgets tighten, they often make cuts in areas like dining out or buying premium liquor. We saw this manifest as some consumers either traded down (opting for less expensive rum brands or smaller bottle sizes) or simply bought less frequently. This particularly affected the lower end “party rums” - heavily price-sensitive customers might shift to cheaper local spirits or even illicit alcohol if branded spirits become too pricey.

However, interestingly, mid-tier standard rums sometimes gained in this environment. If a consumer can’t afford the priciest bottle, they might still avoid the rock-bottom and instead pick a reliable mid-shelf brand. So companies with strong mid-range offerings could capture those switching from both ends (some trading down from premium, others trading up from budget who got a bit more money). Value-for-money became a key selling point. We can expect in 2026, if economic uncertainty continues, that rum marketers will emphasize the quality one can get at a reasonable price - essentially making a case that rum delivers bang for the buck (which can be true; a $30 rum can often be sipped like a whisky twice that price, due to rum’s relative undervaluation historically).

Currency fluctuations and export costs also factor in. Many premium rums are produced in developing economies and priced in USD or EUR in export. If those currencies strengthen or if shipping costs surge, the shelf price in a faraway market can jump, affecting demand. Trade policies (tariffs, etc.) can play a role too - e.g., the EU and U.S. had spirits tariff showdowns in recent years due to unrelated disputes (Bourbon got tariffed in the EU, etc. - fortunately rum was mostly spared but it’s a possibility in any trade war scenario).

Another economic factor: tourism flows. A lot of rum consumption in island producing countries comes from tourists (think beach resorts). If global tourism faces a downturn (due to recession or pandemics), that can hit producers who rely on duty-free or tourist on-site sales. Conversely, a travel boom can boost rum exposure (someone travels to Jamaica, falls in love with Jamaican rum, comes home and continues buying it).

To weather economic storms, rum producers often must be nimble: adjust product sizes (more miniatures or 200ml bottles at lower cost), offer promotions, and ensure supply chain efficiencies to avoid forcing price hikes. Big companies hedge materials and currency to keep pricing stable. Smaller craft producers might focus on direct sales to loyal fans to get through tough times.

Regulatory Complexity and Industry Unity

We’ve already delved deep into the regulatory challenges in the earlier section, so here we will frame it in terms of industry challenge. The lack of unified standards and the ongoing debates around definitions effectively mean rum producers don’t all play by the same rulebook. This can foster mistrust even among producers - e.g., some craft rum makers openly criticize large brands that add sugar or use misleading age statements. Such division isn’t great for overall category marketing; it’s a distraction from promoting rum’s best face. Other spirits sectors have trade associations that very clearly police their own - the Scotch Whisky Association, for instance, would swiftly call out any deceptive practice by a member. Rum’s fragmented oversight means that in some cases questionable practices continue and hurt the category’s reputation among influencers.

On the flip side, we see efforts to unify, like the proposed classification systems and GIs, but these often lack government enforcement or take years to implement. The challenge for 2026 is: can the rum industry come together to at least present a semi-unified front on key issues? One hopeful sign is the increasing voice of rum connoisseurs and journalists - through magazines, blogs (like the influential “The Rum Wonk” who chronicled the Jamaican GI saga), and competitions that set criteria. If the market rewards honest producers (by giving them awards, publicity, and consumer dollars), it naturally pressures others to follow suit or be left behind in the “serious rum” conversation.

Another regulatory challenge is varying tax and distribution laws globally. Spirits taxes are very high in some countries, which can dampen rum sales or make premium rums prohibitively expensive. Any changes (like tax hikes) are a worry for producers. Distribution laws - for instance, states in the U.S. each have their own rules, some control states - can also be a headache, especially for smaller brands trying to expand. While these are broader industry issues not unique to rum, they form part of the complex landscape rum companies must navigate.

In short, the regulatory and self-regulation puzzle is a challenge that overlaps with authenticity (as described). The industry needs to solve how to assure consumers of rum’s quality in a clear, unified way. Doing so will remove one of the last barriers preventing rum from being taken as seriously as whisky or cognac in the fine spirits world.

Facing these challenges, the rum sector in 2026 must be resilient and adaptive. Competition will force innovation and clearer differentiation; economic pressures will reward operational excellence and smart marketing; regulatory complexity (and its gradual resolution) will shape the trust consumers place in rum. The good news is that rum has overcome adversity before - its history includes colonial upheavals, Prohibition, and more - and each time it has found a way to endure and reinvent itself. The current hurdles, while significant, also serve as catalysts for the industry to unify, modernize, and advocate for itself better. How well the rum producers manage these headwinds will determine if the winds fill rum’s sails or blow it off course in the journey through 2026 and beyond.

Conclusion: 2026 Outlook and Beyond

As we set our sights on 2026, the outlook for the rum market is overwhelmingly positive, albeit with a few cautionary notes. The narrative that emerges is one of a category at a crossroads between its storied past and a promising future. On one hand, rum has never been more diverse in offerings nor more aligned with contemporary consumer trends - whether it’s craft premium spirits, flavor exploration, ready-to-drink convenience, or mindful moderation, rum has a play in each space. On the other hand, unlocking rum’s full potential will require continued efforts to overcome its legacy challenges and to differentiate itself amid stiff competition.

So what do we expect in 2026 and the years just beyond? First, continued premiumization appears to be a given. All signs point to premium and super-premium rums growing as a share of the category. We will likely see more ultra-aged releases, more collectors’ editions, and rum further cementing its place on top shelves and in snifters, not just in punch bowls. This will elevate rum’s image and, importantly, its profitability for producers. By 2026, rum might still lag behind whisky or tequila in cachet, but the gap will be narrower if current trends hold. The success of premiumization will also hinge on education and authenticity - delivering “transparent stories around craftsmanship” to consumers, as one 2025 analysis noted. If rum can tell compelling, honest stories about how it’s made and why it’s special, it will win converts for life.

Second, innovation will keep the category fresh. Expect new flavor infusions, cask experiments (perhaps finishing rum in even more unusual barrels, say ex-tequila casks, which would be full circle!), and hybrid products that blur categories. The no/low-alcohol segment likely will expand - who knows, by 2030 we might have a sizable market of “rum-flavored tonics” or similar that become staples for sober-curious consumers. Ready-to-drink cocktails featuring rum will also proliferate, and the brands that ensure these taste authentic and premium will reap rewards. We might even foresee some mergers or acquisitions as big players snap up craft rum distillers or non-alcoholic spirit startups to bolster their portfolios (indeed, the Diplomatico acquisition by Brown-Forman and Diageo’s investment in Ritual Zero Proof signal this trend).

In terms of market performance, the consensus of forecasts suggests that global rum sales will maintain a healthy growth pace through the rest of the decade. We saw projections of around 5% CAGR in value, which, if realized, would take the market to new highs (one estimate puts 2030 global rum at about $18.8 billion, and others that include broader measures put it even higher). That means millions of new cases of rum being enjoyed annually. The growth will likely not be uniform: Europe and possibly parts of Asia might lead in percentage growth, while Asia-Pacific and North America remain volume heavyweights. By 2026, Asia-Pacific will likely still be the largest region, but Europe’s influence as a premium trend-setter will be prominent. The US, if it rebounds with some momentum from its current flatness, could also add significantly to global growth.

Challenges, however, will persist into 2026. Rum won’t magically escape the gravitational forces of the global economy. If inflation or recession worries hit consumers, rum - especially high-end bottles - could see slower growth. The industry will need to stay agile, possibly re-emphasizing affordable luxuries (rum has an advantage here: even top-notch rum is often cheaper than top-notch whisky - a point to communicate to value-seeking connoisseurs). Competition from other spirits will also remain fierce. Tequila’s surge shows no signs of fully abating by 2026; whiskey, with centuries of head start, isn’t ceding its throne. Rum must focus on what makes it distinct rather than trying to be a copy of another category. Leaning into its tropical roots, its cultural richness (the music, the islands, the seafaring heritage), and its sheer fun factor can give rum a brand personality that others can’t easily replicate.

On the regulatory and standards front, the optimist in us would hope that by 2026 some progress is made - perhaps an international agreement on labeling norms or at least a widely adopted voluntary code. If not, the industry should continue self-policing through transparency and building consumer knowledge. In a way, informed consumers become the best regulators: when buyers know what to look for in quality rum, producers will have to meet those expectations or lose market share.