.svg)

.png)

.gif)

Intro

This report was developed by OhBEV, an alcohol marketing agency working at the intersection of brand, data, and culture across wine, spirits, beer, and emerging beverage categories. We created this outlook to move beyond surface-level “trend lists” and provide decision-makers with a clear, experience-driven view of what is actually reshaping the RTD market - from consumer behavior and pricing power to distribution dynamics, regulation, and climate risk.

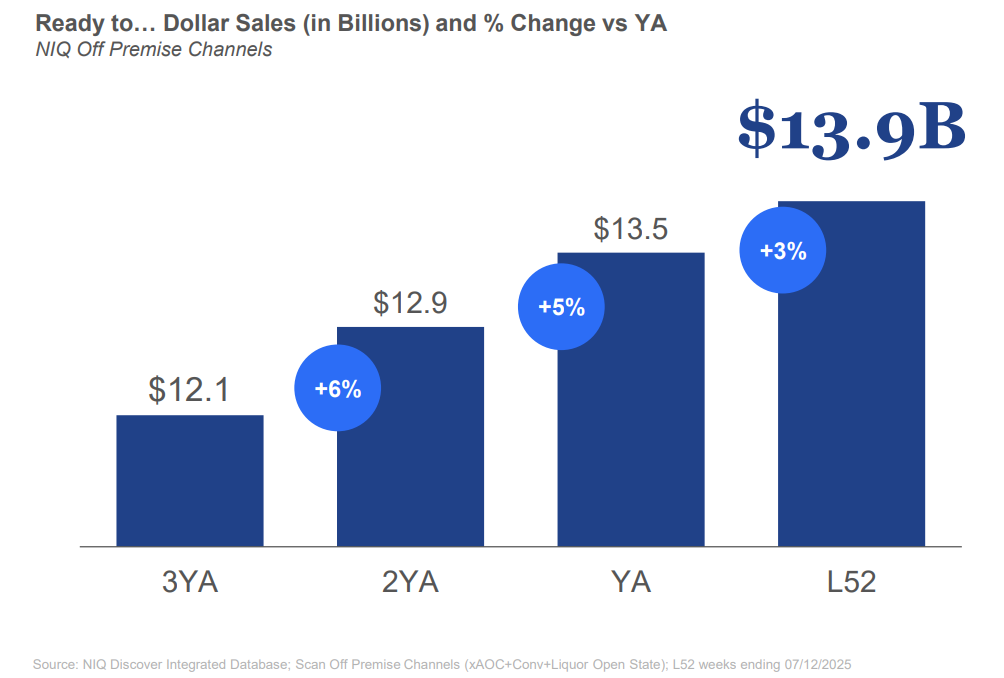

The Ready-to-Drink (RTD) alcohol category continues to be one of the fastest-growing segments in beverage alcohol. Industry data show that RTDs have grown rapidly from a niche into a significant portion of global alcohol sales. For example, IWSR forecasts that RTD volumes across key markets will grow +12% (2022–2027), reaching about US$40 billion by 2027. NielsenIQ reports RTD and RTS (Ready-to-Serve) products now comprise a mature US$13.9 billion global category – roughly 12.5% of all beverage alcohol sales. RTD penetration has risen sharply: in ten leading markets RTDs now account for ~3.5% of all beverage-alcohol servings, up from ~1.1% in 2014. In short, RTDs are here to stay, but growth is becoming more measured as the category matures.

The Macro-Economic Climate and Its Impact on RTDs

Worldwide economic trends and consumer budgets are shaping RTD growth. High inflation and cost-of-living pressures are causing many drinkers to scale back on traditional alcohol purchases. For instance, one of our analysts notes that “with inflation on the rise, many consumers are cutting back on alcoholic beverage consumption” to save money. In this environment, RTDs often serve as an “affordable luxury”: consumers can enjoy premium cocktail flavors at a lower price point. As spending tightens, RTDs act as an entry point to premium spirits at a fraction of bottle prices.

Remarkably, survey data show that in 2023 roughly 45% of alcohol buyers in major markets purchased an RTD in the past year, indicating broad interest despite economic headwinds.

At the same time, some traditional “premiumization” trends are slowing. For example, SipSource data cited in Ansira’s forecasts indicate spirits and wine revenues dipped in late 2024 partly due to rapid RTD growth. In practical terms, many consumers who once traded up within spirits or wine are now redirecting some of that spend into RTD cocktails and long drinks. In sum, the macro backdrop - slower consumer spending growth, inflation, and changing habits - is tempering RTD growth rates, but the category still absorbs spending by offering convenience and value compared to buying individual spirits or wine.

Consumer Participation and Consumption Frequency Trends

RTDs are becoming part of many drinkers’ regular habits. Industry studies report that a large share of consumers try RTDs and many drink them frequently. For example, IWSR research found that 16% of buyers in major RTD markets in 2024 were new to the category (having started drinking RTDs in the past two years). In some countries this was even higher (19% in the UK, 18% in Germany and Canada), suggesting recruitment of new drinkers remains healthy. Meanwhile, frequency of consumption is rising: one IWSR survey showed the share of RTD consumers drinking these beverages more than once per week grew from 39% (2022) to 43% (2023). In other words, existing RTD drinkers are buying them more often.

Consumer surveys corroborate high RTD engagement. In the UK, 41% of consumers report buying premixed alcoholic RTDs, and among RTD drinkers over 50% consume them at least weekly. Notably, the heaviest RTD consumers skew younger and higher-income: e.g. in the UK about one-third of those earning >£75K drink RTDs more than twice a week.

RTD consumption still tends to be at-home, but on-premise use is growing (see next section). Globally, most RTDs are consumed at home or small gatherings, but trends show increasing occasions out-of-home. For instance, 40% of RTD consumers say they are drinking RTDs in pubs more often than a year ago. And in several markets (US, Canada, Australia, South Africa) on-premise RTD volumes have rebounded to pre-pandemic levels. A large base of consumers now include RTDs in their repertoire, with many buying and drinking them regularly as part of everyday occasions.

The Relevance of Ready-to-Serve (RTS) Products

A related category is Ready-to-Serve (RTS) cocktail kits or larger-format mixed drinks. RTS gained attention during COVID as home cocktail-making soared. RTS products were largely a U.S. phenomenon and came to market in response to the at-home cocktail occasion. However, many analysts observe RTS has peaked: new launches have tailed off after a pandemic peak. RTS drinks often carry higher ABV and are sold in shareable formats (500 ml+ bottles) – effectively premiumizing RTDs. Indeed, RTS is seen as a premiumization lever, especially in the on-trade: these larger cocktails help bars lacking mixology staff still offer cocktails.

The U.S. leads in RTS activity; other markets remain nascent. RTS is most popular in the U.S., with brands such as Tarquin’s Gin and Three Olives launching multi-serve cocktails. In practice, brands offering RTS cocktails often highlight their cocktail-accurate flavors and higher ABV. For example, many RTS launches are cocktails with higher alcohol content (often 10–12% ABV) sold in both single-serve cans and larger bottles. In conclusion, while RTS is a smaller sub-category, it remains relevant for high-end occasions: it allows brands to capture special occasions and bar segments even as overall launch pace has cooled.

Importance of Alcohol Base in RTD Selection

The type of alcohol base (malt, wine, spirits) is a key choice factor for RTD drinkers. Multiple sources confirm consumers care about base. An alcohol base is now the joint-second most important factor in RTD selection. NielsenIQ shows that spirits-based RTDs are outperforming other bases. Globally, spirit-based RTD volumes have grown, while wine- and malt-based RTDs have declined: in 2022 spirits-RTDs were +5% versus -3% (wine) and -4% (malt). In many markets, spirit-based RTDs carry a premium: up to 25% of RTD drinkers say they would pay more for a spirit-based RTD than a malt one. Vodka remains the most popular spirit base, but tequila is rising in prominence.

The dominance of spirits is especially pronounced in cocktails and hard seltzer segments. For example, Nielsen reports that in the U.S. In the RTD cocktail-shots category, malt-based formulations have the largest share (48.2% in 2026), but spirits-based RTDs (24.0%) command a premium positioning. Malt base dominates the niche market (just under half share), underscoring the regulatory and cost advantages malt brings (lower tax in many states). Still, overall market trends point to consumers valuing authenticity: spirit bases score highly for perceived quality, especially among young drinkers.

Consumer Confusion About Alcohol Bases

Paradoxically, many RTD consumers misunderstand the alcohol base of products. For instance, a majority of drinkers misattribute hard seltzers. Although most hard seltzers are malt-based (about 83%), 54% of consumers assume hard seltzer is spirits-based. This mismatch suggests that packaging, marketing, and naming conventions (e.g. “vodka soda” vs “hard seltzer”) can mislead buyers. Similarly, some wine-based RTDs and spritzers are consumed without drinkers realizing the base spirit/wine content.

This confusion can impact brand choice. It means that consumers may make decisions based on perceived base (and price) which do not match product reality. For brands, it underscores the importance of clear labeling and education. Products with a branded spirit base are underperforming versus RTDs with an unbranded spirit base, indicating that the base confusion and branding can shape performance. In practice, educating consumers about base (and thus setting expectations) can be a strategic advantage (see Takeaways).

Maturity of RTD Segments and Innovation Efficiency

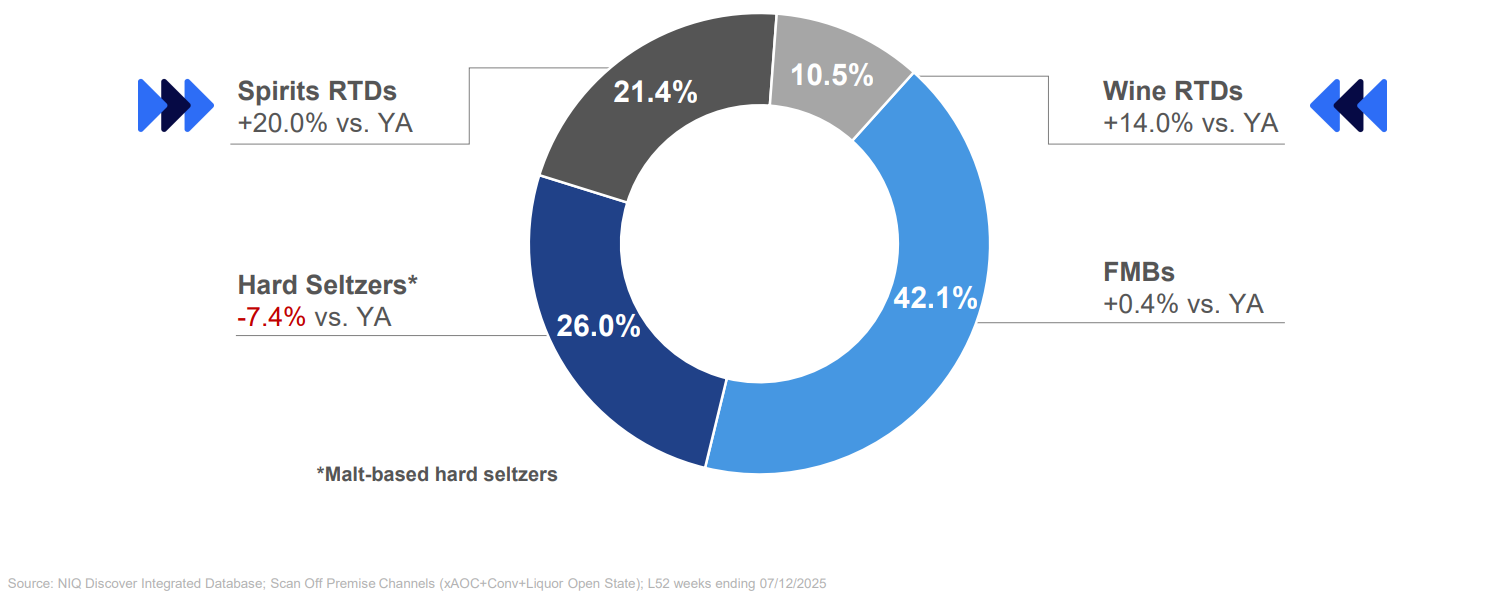

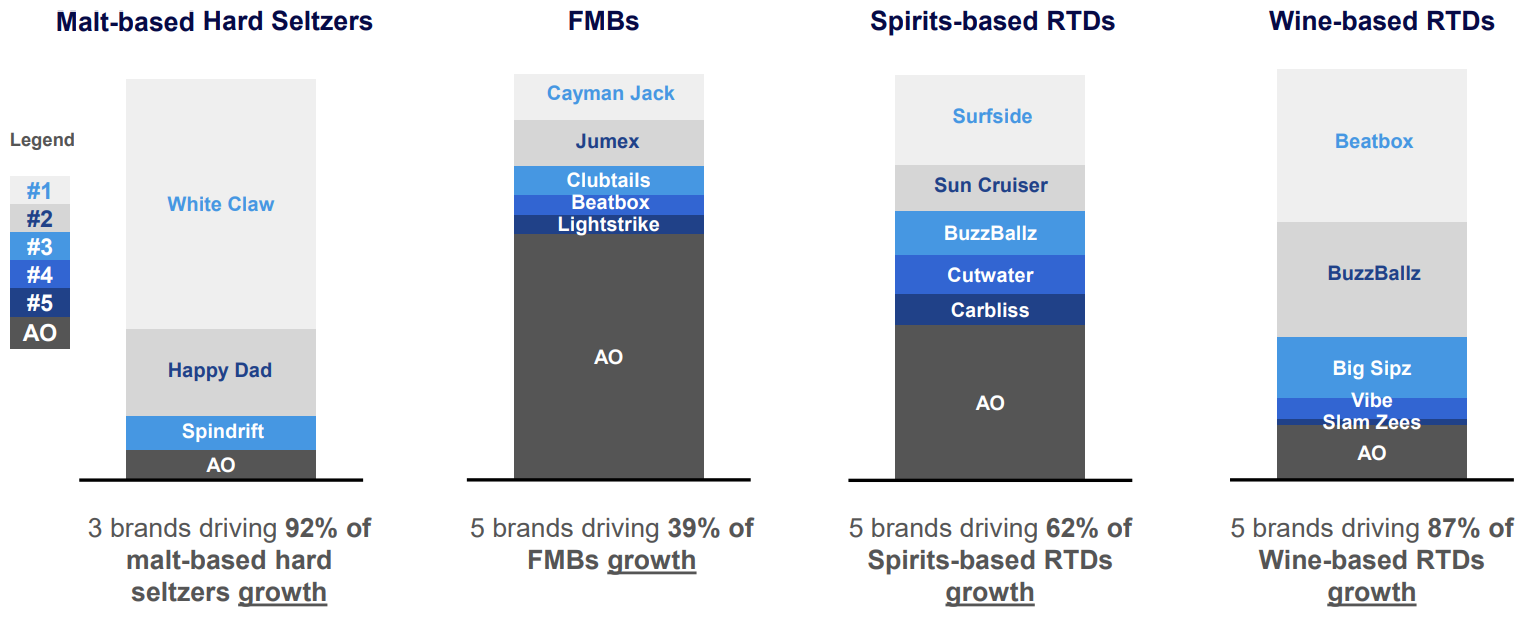

Many RTD subcategories are reaching maturity. The overall RTD growth is decelerating and innovation is slower. In particular, the hard seltzer craze has cooled: hard seltzers are down -7.4% in the latest period, whereas spirits-based RTDs are up +20% and wine-based RTDs +14%. This indicates a shake-out of once-hot niches.

Innovation is also becoming more efficient (albeit at a smaller scale). The RTD new-product launches peaked in 2021 and have since collapsed: in 2021 the category saw over 3,300 new RTD products launched globally, but in the first half of 2024 there were fewer than 1,000. This drop means fewer new flavors cluttering shelves, but it also raises the bar for each launch’s impact. While launch volumes have shrunk, the effectiveness of new launches has improved, as producers are more strategic and targeted.

In sum, the RTD category is consolidating. Brands are focusing on fewer, bigger innovations – e.g. high-ABV cocktails, premium ingredients – rather than endless variations. However, retailers are also imposing discipline: shelf space is tight, so only truly differentiated RTDs survive. Flavor fatigue is real, and many markets are now saturated. This maturity means growth must come more from existing product improvements and channel expansion than from a flood of new SKUs.

Rethinking RTD Launches

Given the crowded RTD shelf and cautious consumers, “me-too” launches are less viable. Experts advise that innovation must have a compelling point of difference. The new baseline is differentiation – me-too products will not cut it. Brands must identify unique selling points (distinctive flavors, formats, or brand stories) to stand out. For example, launching RTDs with premium spirits (tequila, rum) or unique regional cocktails can draw interest.

Additionally, product lifecycles must be planned carefully. Brands should phase out underperforming flavors and streamline portfolios. The focus should be on innovation efficiency: introducing fewer products that truly meet an identified consumer need. While launch counts have plummeted, less reliance on innovation to drive performance has not stopped growth. The key is ensuring new releases are effective and resonate with consumers. In practice, successful RTD brands often concentrate on a stable of core products with occasional line extensions, rather than over-diversification.

The On-Trade Channel: A Growing Frontier for RTDs

Traditionally, RTDs sold mostly off-premise (in stores and online). However, the on-trade (bars, restaurants, pubs) is emerging as a prime growth area. Several factors drive this shift: younger consumers are more likely to order RTDs when socializing, and bars appreciate the speed and profit of canned cocktails. 40% of consumers say they are drinking RTDs in pubs or bars more often than last year. This reflects a real uptick in on-trade RTD occasions.

In markets like the US and Canada, on-premise RTD volume has fully recovered to or above pre-pandemic levels. Bars and clubs are stocking hard seltzers, malt cocktails, and even spirits-based RTDs to meet demand.

In Brazil, China, and South Africa, drinkers are notably shifting RTD consumption to on-trade venues – possibly because younger demographics in those countries frequent bars more often. For RTD brands, this means new marketing and distribution strategies: rather than only selling in retail, they should build relationships with bars, update packaging (e.g. bulk formats for bars), and even train bartenders to feature RTDs as mixed-drink alternatives. The on-trade offers both volume growth and higher margins for RTDs, making it a key frontier.

Spirits and RTDs Gaining Share from Wine

A notable trend is RTDs encroaching on wine’s territory. The RTDs are gaining share not just from beer, but also from still wine. Globally, as RTD consumption has risen from 2019-2024, still wine consumption has fallen. The RTDs doubled their share of global beverage serves from 1% to 2% over 2019–2024, while still wine’s share slipped from 11% to 10%. This gap is even more pronounced in high-growth markets: in the US RTD volumes grew at +14% CAGR (2019–2024) while still wine volumes declined ~4%. By volume, RTDs in the US now exceed all wine (still + sparkling) combined. Similar patterns appear in Japan and Canada.

The softening of wine may reflect changing preferences: younger drinkers often find RTDs more convenient and socially engaging than a bottle of wine. It also reflects health and moderation messaging; some RTDs are marketed as “light” or “low calorie” alternatives. In practical terms, wine producers are watching RTDs closely. Canada and Australia RTDs are on track to surpass wine volumes in the next few years.

While RTDs eat into wine’s market share, interestingly some hybrid innovation is occurring (e.g. wine spritzers, canned wine-cocktails). But overall, the wine category is losing ground to RTDs, especially as RTDs continue to innovate faster and tap the social-media zeitgeist more effectively.

Spotlight on 2026 Launches

New RTD products keep pouring onto the market, often reflecting the latest trends. Recent announcements highlight several themes:

- Flavor collaborations and nostalgia. Just Call Me Shirley (a craft RTD brand) launched vodka and tequila versions of its “Dirty Shirley” canned cocktail. Inspired by the classic Shirley Temple, this brand emphasizes premium spirits and nostalgia (no artificial dyes).

- Premium spirit-based cocktails. Small companies like Subourbon Life are expanding bourbon-based RTDs with novel flavors (Bourbon Piña Colada, Bourbon Espresso Martini). These aim to make high-quality bourbon cocktails accessible and fun in convenient packaging.

- Functional and non-alcoholic options. Health and mood-focused products are also coming: UK’s Smiling Wolf released a line of alcohol-free canned cocktails (G&T, Spritz, Mojito, Negroni) infused with nootropics and vitamins for energy and relaxation.

- Big-brand entries. Major brands continue to launch RTDs. For example, Brown-Forman is bringing New Mix (Mexico’s top tequila RTD) to the U.S., offering El Jimador-based Paloma and Cantarito canned cocktails. Similarly, Malibu (rum) partners with Dole to debut pineapple-flavored rum cocktails in the U.S. (pineapple, mango, etc.) in 2026.

- Global imports and local twists. Across regions we see both global hits and local innovations. (E.g. liqueur brand Passoã launched passion-fruit RTD cocktails in Europe.)

These 2026 launches reinforce key trends: brands emphasize interesting flavor combinations, premium or craft credentials, and the expansion of both alcoholic and alcohol-free segments. The variety of new products suggests RTD innovation is broadening beyond hard seltzers into classic cocktails, global flavors, and functional wellness.

Key Markets Analysis

United States

The U.S. is the largest RTD market globally. RTDs hold roughly 8% of all beverage-alcohol servings in the U.S. (and Canada). Growth has moderated: U.S. RTD volume was up only about +1% in 2024, and forecasts suggest roughly 1% annual CAGR into 2029. Nonetheless, the U.S. market is diversified and innovative. Hard seltzers (which exploded a few years ago) have come off their peak, but cocktails/long drinks and hard tea are gaining share. In practice, popular American RTDs include flavored malt beverages (e.g. Bang Energy’s new line), spirits-based cocktails (e.g. Cazadores Hard Soda – tequila-infused seltzer), and canned cocktails targeting older millennials (e.g. New Mix tequila cocktails). Many U.S. brands are premiumizing: higher ABV, cleaner labels, and craft packaging.

Channel-wise, convenience and liquor stores remain important, but on-premise (bars, clubs) is rebounding (40% of drinkers report more pub consumption). Domestic production is strong, though recent tariffs have raised costs on imported RTDs. In summary, the U.S. RTD market is mature but still innovative, with heavy competition driving premiumization and new flavors (e.g. hard kombuchas, RTD coffee, etc.).

Italy

Italy’s RTD market is comparatively small and has seen slow growth or slight decline. Italian RTD volumes fell ~2% in 2024 (about -1% CAGR since 2019). Still wine, Italy’s traditional forte, is also declining (-3% CAGR 2019–2024). By most forecasts, the category is expected to remain flat to modest in Italy through 2026. RTDs in Italy tend to skew toward aperitivo-style drinks (e.g. bottled spritz) and imported cocktail brands. Consumer surveys suggest limited interest: only ~1% of Italian still-wine drinkers would choose a premixed cocktail if wine were unavailable. This reflects Italy’s deep wine and cocktail culture. In short, RTDs are growing slowly in Italy, and most growth to 2026 will come from niche innovation (like local vermouth-based RTDs) and on-trade adoption (bars offering bottled cocktails) rather than major market disruption.

France

France’s RTD market is relatively underdeveloped. Available insights suggest modest growth – one market report projects roughly +1-2% annual volume growth through 2026, indicating a very gradual expansion. French consumers traditionally favor wine, so RTDs currently play a small role. Some RTDs (flavored canned cocktails or spritzers) are gaining traction among younger Parisians, but nationwide RTD share remains low. Regulatory factors (strict wine & spirits laws) also limit RTD diversity. Overall, expect slow growth in France: niche premium RTDs and alcohol-free versions may find urban appeal, but RTDs are not yet a major category in 2026. (No direct citations found; anecdotal industry reports indicate France’s RTD CAGR ~1.6% through 2026.)

China

China is one of the most promising RTD markets. We forecast ~+6% volume CAGR (2022–2027) for Chinese RTDs. Growth is driven by urban consumers experimenting with Western-style drinks and by domestic brands introducing novel formats. However, recent year-on-year figures are volatile: in 2024 China’s RTD volume actually fell ~14% (likely after an earlier surge). This suggests short-term softness, but long-term potential remains strong due to China’s size and rising cocktail culture. Key trends in China include flavored alcoholic beverages (local fruity drinks) and RTDs targeting night-time leisure venues. By 2026, China’s market is expected to become a significant slice of global RTD sales, propelled by its large population and growing middle class.

Brazil and South Africa

Brazil and South Africa are rapidly expanding RTD markets. Both registered ~+12% volume growth in 2024, making them among the world’s fastest-growing. In Brazil, local flavors and social occasions (e.g. beach, Carnival) are leading RTD uptake; major distillers and breweries are ramping up RTD lines (e.g. vodka sodas, cachaça cocktails). In South Africa, a younger drinking demographic and popularity of gin/rum cocktails have fueled RTD adoption. We forecast mid-single-digit CAGR in these markets through 2029, but many consumers are still new to RTDs. These “emerging” markets have low RTD penetration today, so growth comes more from category building (educating consumers, expanding distribution) than incremental shifts from other alcohol. In both countries, on-trade and cold-chain retail are important – e.g., RTDs are sold widely through convenience stores and taverns. Overall, Brazil and South Africa will be key engines of RTD volume growth into 2026.

Regulatory Momentum: RTD Policy Outlook in 2026 and Beyond

Government policies are beginning to catch up with the RTD trend. In the U.S., trade and licensing reforms could significantly impact RTDs. In 2025 new tariffs were imposed on imported goods: most EU beverages (including RTDs) now carry a flat 15% import duty, up from nearly 0%. This raises costs for imported RTDs (especially spirits-based ones from Europe) and may accelerate the shift to domestically produced or private-label RTDs. Notably, in mid-2025 the U.S. and EU agreed to a 15% “zero-for-zero” baseline, but full exemptions for alcohol are still under discussion. Brands will need to watch this closely, as duties could squeeze margins or encourage reshoring.

On the regulatory front, U.S. states are liberalizing RTD distribution. Several states are updating laws that historically treated spirits-based RTDs differently from beer and wine. For example, Texas is considering SB2255, which would allow spirits-based RTDs (≤17% ABV) to be sold in grocery and convenience stores starting in September 2025. Alabama recently authorized low-ABV spirits RTDs in supermarkets, and similar bills are proposed in Florida, Pennsylvania, and Michigan. This trend reflects industry and consumer pressure to “level the playing field.” According to trade groups, about two-thirds of U.S. consumers support allowing spirits-based RTDs alongside beer/wine in retail. If enacted, these changes would dramatically expand retail access for RTDs in major markets.

Outside North America, specific RTD policy moves are less prominent in our sources. No new EU-wide regulations on RTDs have been announced, though standard excise taxes and labeling rules still apply. In markets like Australia, longstanding beer/malt RTD taxes are being re-evaluated, but any changes appear incremental. In summary, the key policy stories for RTDs in 2026 are the evolving U.S. tariffs and state alcohol laws – both of which brands must monitor and adapt to in pricing, supply chain, and distribution planning.

Strategic Considerations for Brands and Marketers in 2026

To succeed in the maturing RTD market, brands should adopt several strategic imperatives:

- Product Differentiation and Innovation Focus. With “me-too” products unlikely to succeed, prioritize unique flavors, formats, and branding. Leverage high-interest bases like tequila or exotic botanicals. Ensure new RTDs offer something distinct (e.g. functional ingredients, premium spirits, novel flavor twists). Don’t over-launch; instead focus on quality over quantity so each new product stands out.

- Alcohol Base Transparency. Address the confusion gap by being explicit about the RTD’s base. Clear labeling (e.g. “Vodka Soda RTD,” or country-of-origin emphasis) can build trust. Educate consumers through marketing (in-store signage, digital content) about the base, to capture the willingness to pay more for spirits-based RTDs. Differentiating on base can reinforce premium positioning.

- Value Proposition and Pricing. In a cost-sensitive environment, emphasize affordability and value without sacrificing perceived quality. Offer “affordable luxury” messaging – highlight premium ingredients or craft processes to justify a slightly higher price point. Monitor tariffs and production costs closely; consider private-label partnerships or in-region production to maintain competitive pricing.

- On-Trade Activation. Invest in the growing on-premise channel. Develop RTD cocktails tailored for bars and restaurants (e.g. batch formats for quick pour, branded glassware). Build relationships with mixologists to feature your RTDs on tap or in cocktails. Design point-of-sale materials for pubs to promote RTDs as premium grab-and-go or cocktail substitutes. (on-trade RTD volume has recovered in many markets, so fighting for presence here is crucial.)

- Consumer Engagement & Fatigue Management. Use market research to understand local tastes (by market/region) and adjust portfolios accordingly. Avoid over-saturating shelves; rationalize SKUs to core winners. Consider targeted loyalty programs or social media campaigns to reinforce top products. Since brand loyalty is often low, storytelling and authenticity (founder story, local ingredients) can help differentiate in a fragmented market.

- Packaging and Convenience. Leverage consumer trends for convenience. The majority of RTDs are in cans or on-the-go packs. For example, in the U.S. cans already hold 57.4% of the RTD cocktail shots segment. Consider formats that fit consumers’ lifestyles (cans, pouches, multi-serve bottles). Highlight portability and eye-catching design – on-shelf appeal is a key trial driver (especially for impulse purchases).

- Economic Preparedness. Plan for uncertain economics. Model how potential tariff or tax changes could affect costs. Build inventory buffers or flexible supply chains to handle disruptions. If costs rise, decide which SKUs to trim or whether to introduce smaller pack sizes. Communicate any price changes transparently to retain consumer trust.

- Data-Driven Planning. Continually gather and analyze sales data and consumer feedback. Use insights (OhBEV, Nielsen, IWSR, syndicated surveys) to spot emerging trends (e.g. new flavor preferences, demographic shifts). Share these insights across R&D and marketing teams to stay ahead of the curve.

By addressing these areas – innovation, value, channel strategy, consumer insight and regulatory preparedness – RTD brands can navigate the challenges of 2026. The emphasis should be on smart, targeted growth rather than broad risk-taking, ensuring resources focus on the most promising opportunities.

Planning for 2026

For the coming year, RTD companies should actively incorporate industry intelligence into their plans:

- Leverage Market Insights. Stay informed with the latest research (such as OhBEV, IWSR, NielsenIQ, and trade reports) on consumer behavior and forecasted trends. Identify which sub-categories (e.g. hard kombucha, cocktail shots) are expanding.

- Invest in Relevant Innovation. Develop products aligned with consumer trends (e.g. low-sugar, organic, or novel flavors). Prototype with targeted consumer testing – there’s still room for new formats like pouch cocktails or alcohol-free blends that maintain RTD convenience.

- Strengthen Brand Messaging. Clearly articulate the brand’s story and value: emphasize premium ingredients or sustainability efforts. Use digital marketing and social media to reinforce messages. Tailor messaging to local markets (e.g., different campaigns in the U.S. versus Europe based on taste differences).

- Expand Channels. Explore new distribution, including e-commerce, subscription boxes, and on-demand delivery. Off-trade is still growing (supermarkets, convenience stores), but also pursue partnerships with foodservice chains and hotels. Prepare for omnichannel marketing: ensure consistent branding online and offline.

- Set Realistic Sales Targets. Given slower overall growth, set achievable targets for each SKU. Prioritize core products for reorders, and treat any new product launch as an investment with defined milestones (trial rates, repeat purchase targets).

- Monitor Regulations. Keep an eye on upcoming policy changes (tariffs, licensing laws) and incorporate scenarios (e.g. higher import taxes) into financial planning. Engage with industry associations (e.g. DISCUS) to stay abreast of legal developments.

By combining data-driven planning with nimble execution, brands can better align their 2026 strategies with the evolving RTD landscape.

Conclusion

The Ready-to-Drink market in 2026 is both dynamic and mature. Consumers have broadly embraced RTDs as convenient, flavorful alternatives to traditional spirits and wines, driving substantial category growth over the past five years. Yet the pace of expansion is now moderating: innovation is more targeted, and market penetration is deepening rather than exploding. Younger demographics and the “sober-curious” movement have injected new energy into RTDs, but macroeconomic pressures (inflation, cost-cutting) mean drinkers choose RTDs more deliberately.

Importantly, RTDs - especially spirits-based - continue to gain share at the expense of wine and beer. As noted, RTDs’ global serving share doubled (1% to 2%) between 2019 and 2024, while still wine’s share fell. This suggests a long-term trend: RTDs are carving out a significant and growing niche. The on-trade channel is a key frontier: bars and restaurants are increasingly stocking RTDs, creating new occasions.

Looking forward, industry forecasters remain optimistic. We project that global volumes of cocktail and long-drink RTDs will roughly double between 2019 and 2029, with North America potentially seeing up to a 400% increase in RTD cocktail servings. This underscores that, despite current headwinds, the long-term outlook is strong. Brands that adapt to the shifting landscape - by understanding the importance of alcohol base, targeting emerging consumer segments, and innovating smartly - will be well-positioned. The coming year will reward those who can balance growth ambitions with efficiency, staying close to consumer trends while navigating regulatory and economic changes.

Key Takeaways for Brands and Marketers

- Educate on Alcohol Base. Use clear labeling and marketing to align consumer perceptions with actual product base. This builds trust and allows premium base choices to command value.

- Target Growing Demographics. Focus on attracting younger legal drinkers (Gen Z/Millennials), who are driving much of the new RTD demand. Tailor flavors and branding to resonate with their tastes and values.

- Prioritize Strategic Innovation. Emphasize quality and distinctiveness in new products. Better to launch fewer, well-designed RTDs that meet specific needs (flavor, occasion, health) than to flood the market with minor variants.

- Reinforce Core Products. In a fatigued market, bolster existing best-sellers (e.g. by refreshing packaging or marketing) rather than overextending the line. Use variety packs or seasonal limited editions to keep interest without fragmenting the core range.

- Leverage On-Trade. Develop partnerships with bars and restaurants. Create RTD offerings specifically for on-premise (kegs, batch cocktails, or cocktail lists) to expand reach and consumer trial.

- Balance Price and Value. In a cost-conscious era, ensure RTD pricing reflects value. Consider smaller pack sizes or promotions to retain budget shoppers, while upholding quality branding for premium lines.

- Use Data-Driven Strategy. Continuously monitor industry reports and sales data. Consumer tastes shift quickly in RTDs, so timely market intelligence is crucial for planning and pivoting.

By focusing on these strategic areas, RTD brands can navigate the evolving landscape and capture growth opportunities. An adaptable, consumer-centric approach will be the key to thriving in the dynamic RTD market of 2026 and beyond.

.svg)